The latest United Kingdom Consumer Price Index (CPI) data shows headline inflation at 2.8% year-over-year in May, unchanged from April, according to the Office for National Statistics (ONS). In this article, Nummixo brokers deliver a detailed and reader-friendly overview of the subject matter.

While stability in the inflation rate may appear neutral on the surface, the level remains significantly above the Bank of England (BoE) 2.0% inflation target, confirming that disinflation progress has stalled at elevated levels rather than accelerating toward target convergence.

From a macro pricing perspective, a sustained 2.8% CPI regime implies that inflation remains embedded above equilibrium, particularly when measured against the BoE’s policy-consistent band closer to 1.5%–2.0%. This keeps real rates under constant recalibration pressure, especially if nominal yields fail to adjust in tandem with sticky services inflation.

Core Inflation and Monthly Momentum Deceleration

The core CPI index, excluding volatile food and energy components, printed at 2.6% YoY, up marginally from 2.5% in April, but below the consensus expectation of 2.7%. This 10 basis point deviation from the forecast suggests that underlying inflation pressures are not accelerating at the expected pace, despite remaining structurally elevated above pre-pandemic norms.

On a sequential basis, monthly CPI rose only 0.2% in May, sharply lower than the 0.7% expansion recorded in April. This represents a 500 basis point deceleration in monthly inflation momentum, and below the expected 0.4% print, indicating that short-term price pressure is losing velocity.

From a statistical inflation tracking perspective, this divergence between sticky annual inflation (2.8%) and weak monthly prints (0.2%) signals a potential base effect distortion combined with cooling demand elasticity.

Monetary Policy Transmission and BoE Rate Path Sensitivity

The Bank of England policy reaction function remains highly sensitive to deviations in CPI from the 2% inflation anchor, particularly in the core and services sub-components. With inflation at 2.8%, the policy stance remains restrictive, but the latest data reduces the probability of additional tightening cycles.

From a rate-path pricing perspective, money markets are increasingly sensitive to the distribution between terminal rate expectations and first-cut timing scenarios. A stable headline CPI combined with weaker-than-expected monthly momentum typically reduces the implied probability of further hikes and increases the weighting toward rate stability followed by gradual easing assumptions.

However, the persistence of inflation above 2.5% YoY still limits the BoE’s flexibility, as premature easing could risk re-anchoring inflation expectations above target. Therefore, the current CPI regime supports a higher-for-longer plateau structure, rather than immediate policy reversal.

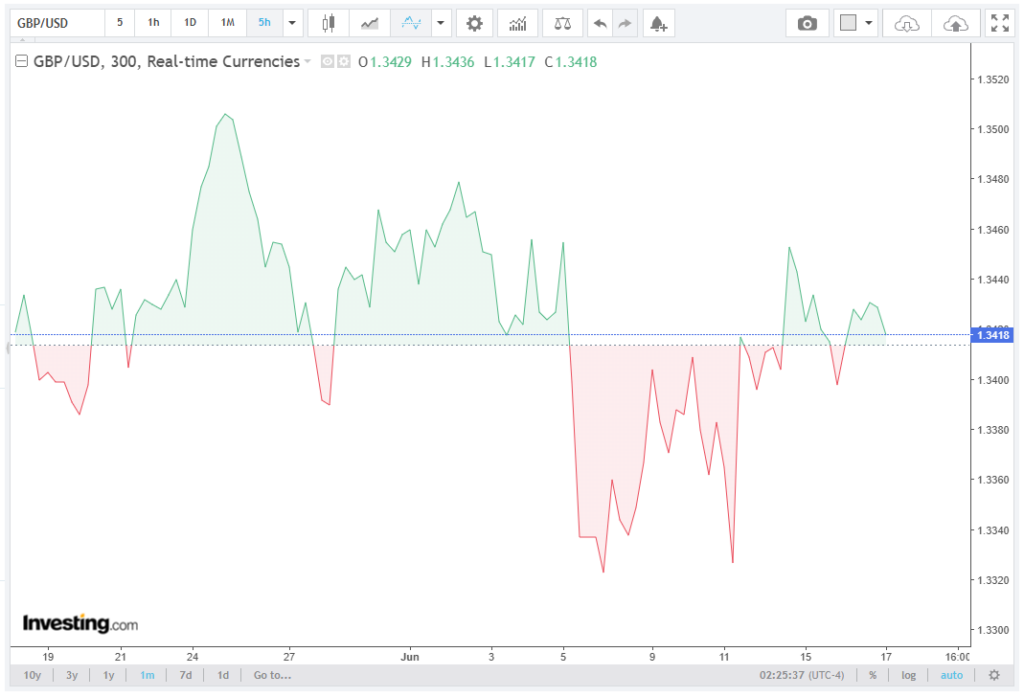

Technical Structure: GBP/USD Consolidation Regime

From a technical standpoint, GBP/USD is exhibiting a neutral consolidation structure, with price action confined within a Bollinger Band compression regime and capped by the 100-day simple moving average (SMA).

The pair trades marginally above the Bollinger mid-band at 1.3420, which is acting as a short-term equilibrium pivot. The 100-day SMA at 1.3460 continues to function as dynamic resistance, reinforcing a ceiling that has contained multiple upside attempts.

Momentum indicators confirm this neutral structure. The Relative Strength Index (RSI) near 50 reflects equilibrium conditions, with neither bullish nor bearish divergence present. Volatility contraction suggests the market is in a mean-reversion phase rather than a trend expansion phase, typically preceding a directional breakout once volatility re-expands.

Key Technical Thresholds and Volatility Bands

On the upside, immediate resistance is defined by the 100-day SMA at 1.3460, followed by the Bollinger upper band near 1.3498, which represents the upper volatility boundary of the current compression channel. A sustained break above this zone would signal a volatility expansion phase with bullish continuation potential.

On the downside, initial support is located at the Bollinger mid-band around 1.3420, which currently acts as a short-term equilibrium anchor. A breakdown below this level exposes the Bollinger lower band near 1.3345, where liquidity concentration and potential mean-reversion buying interest may emerge. A decisive break beneath 1.3345 would indicate a shift toward a broader corrective regime with downside momentum acceleration.

Macro-Financial Outlook

The combination of 2.8% sticky headline inflation, moderating monthly CPI momentum at 0.2%, and sub-forecast core inflation at 2.6% YoY defines a macro environment characterized by inflation stabilization rather than reacceleration or full normalization.

For the British Pound, this translates into a range-bound macro regime, where directional conviction remains limited, and FX pricing is increasingly driven by external yield dynamics and technical positioning rather than domestic inflation shocks.

Unless CPI decisively breaks either above 3.0% (inflation risk repricing) or below 2.5% (disinflation acceleration), GBP/USD is likely to remain structurally neutral with compression-driven price behavior dominating near-term flows.