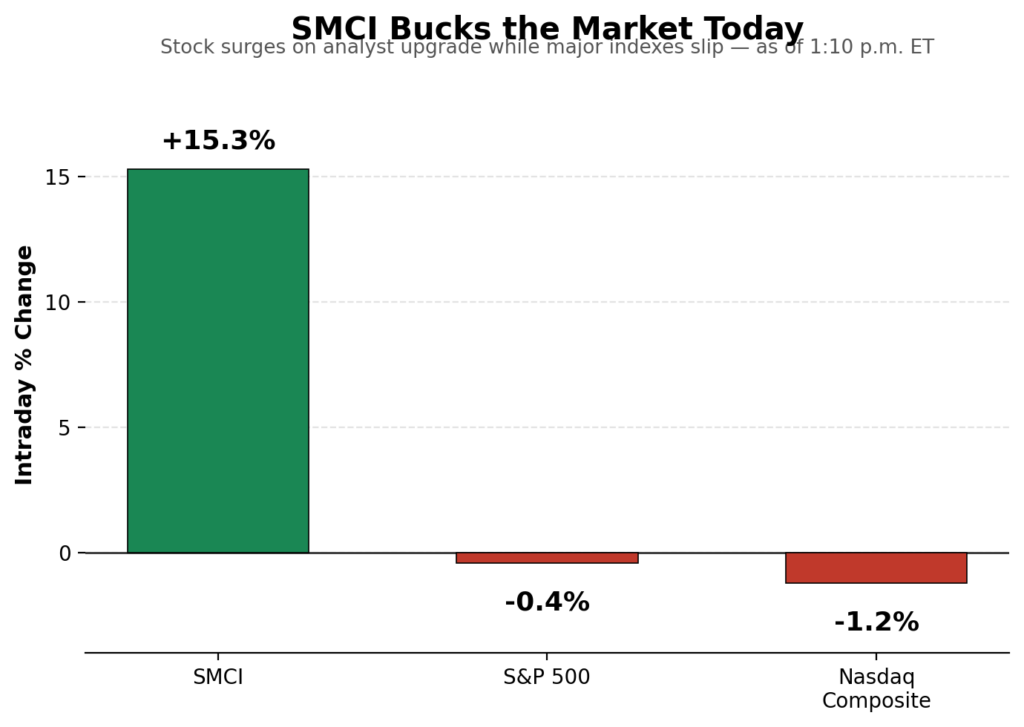

Super Micro Computer (SMCI) stock is surging today, up as much as 17.71% intraday and still showing a 15.3% gain as of 1:10 p.m. ET a striking move against a broader market that’s actually moving in the opposite direction, with the S&P 500 down 0.4% and the Nasdaq Composite off 1.2% on the same day.

Brokers from Eidellux have been tracking what’s driving the divergence, and the short answer is a single, well-timed piece of analyst coverage.

An upgrade lit the fuse

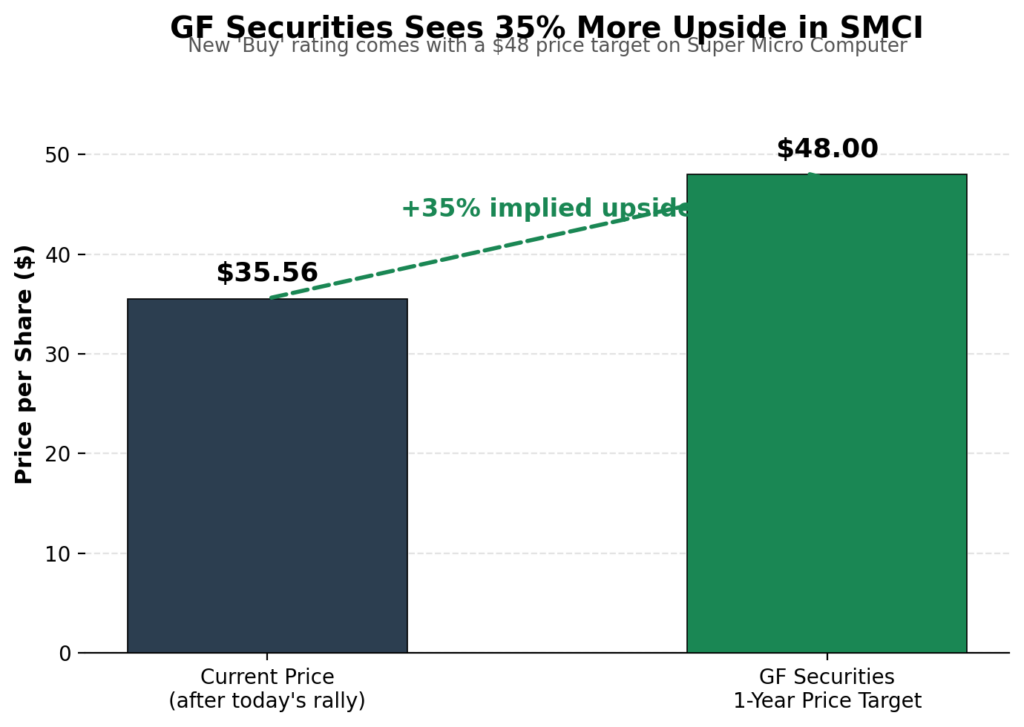

GF Securities published a research note on Supermicro before the market opened this morning, upgrading the stock from hold to buy. That single rating change appears to be the primary catalyst behind today’s rally. With the day’s gains included, Supermicro shares are now up roughly 21% for the year, a meaningful turnaround for a stock that’s had a volatile 12 months.

The note didn’t stop at a simple rating bump. GF Securities set a one-year price target of $48 per share, which, even after accounting for today’s sharp move higher, still implies an additional 35% upside from current levels. That’s an aggressive call from a firm that, until this morning, had been sitting on the sidelines with a neutral rating.

Why GF sees an attractive entry point

Part of what makes this upgrade notable is the timing relative to Supermicro’s recent stock performance. The company’s announcement that it planned to raise $7 billion through a new share sale had triggered a significant pullback in the stock, as investors weighed the dilution impact of issuing that much new equity. GF’s analysts appear to view that pullback as having created the attractive entry point referenced in their note, rather than as a lasting concern.

The firm’s bullish thesis also leans on an external demand driver: continued ramp-up in AI infrastructure spending from Space Exploration Technologies (SpaceX). As SpaceX and other large AI players continue scaling compute infrastructure, GF sees Supermicro positioned to capture a meaningful share of that spending growth through its server hardware business.

The bull case: AI servers remain in high demand

Strip away today’s headline-driven pop, and the underlying bull case for Supermicro centers on its position in the high-performance AI server market. Demand in this category has continued to climb as hyperscalers and AI labs build out data center capacity, and Supermicro has established itself as one of the more prominent hardware suppliers serving that buildout.

If AI infrastructure spending continues at its current pace and SpaceX’s ramp is one data point suggesting it will, Supermicro stands to benefit directly as one of the picks-and-shovels suppliers behind the broader AI trade.

The risk side: legal and governance overhang

The bullish growth narrative does not tell the entire story. A key reason Supermicro’s stock has traded so inconsistently over the past year is the ongoing scrutiny surrounding reports linking individuals associated with the company to the alleged export of restricted AI hardware to China.

These allegations have created a persistent overhang on investor sentiment, regardless of the company’s underlying business performance and demand trends. In fact, the uncertainty surrounding these issues is a major reason why the stock has often traded at a discount compared with its growth potential.

As a result, today’s rally is occurring against a backdrop of unresolved legal and management-related risks. These risks may not be reflected in quarterly earnings results, but they have the potential to re-emerge suddenly through new reports, regulatory investigations, enforcement actions, or additional disclosures. For investors, this means that strong growth prospects and elevated headline risk continue to coexist, making the stock’s risk-reward profile more complex than its recent price action alone might suggest..

Outlook: cheap valuation, real risk attached

Taken as a whole, Supermicro’s valuation appears to understate its potential growth in the rapidly expanding AI server market, which is the core premise behind GF Securities’ recent upgrade.

The firm’s $48 price target, implying approximately 35% upside, reflects confidence that the company’s position within the AI infrastructure ecosystem will continue to drive strong growth. Additionally, the recent capital raise that initially concerned investors may ultimately prove insignificant if the company delivers on its growth expectations.

However, investors should not overlook the risks. Legal and corporate governance concerns related to export-control allegations remain unresolved, and these issues cannot be assumed to be fully reflected in the current share price simply because the stock has rallied.

For investors evaluating Super Micro Computer, the situation can be viewed as a balance between meaningful upside potential and genuine headline risk. While the company’s AI-driven growth story remains compelling, today’s stock gains do not eliminate the uncertainties surrounding regulatory and governance matters, leaving both opportunities and risks firmly in play.