Bristol Myers Squibb (BMY) shares have gone essentially nowhere for the past several years, and the reason comes down to two words that strike fear into pharmaceutical investors: “patent cliff.”

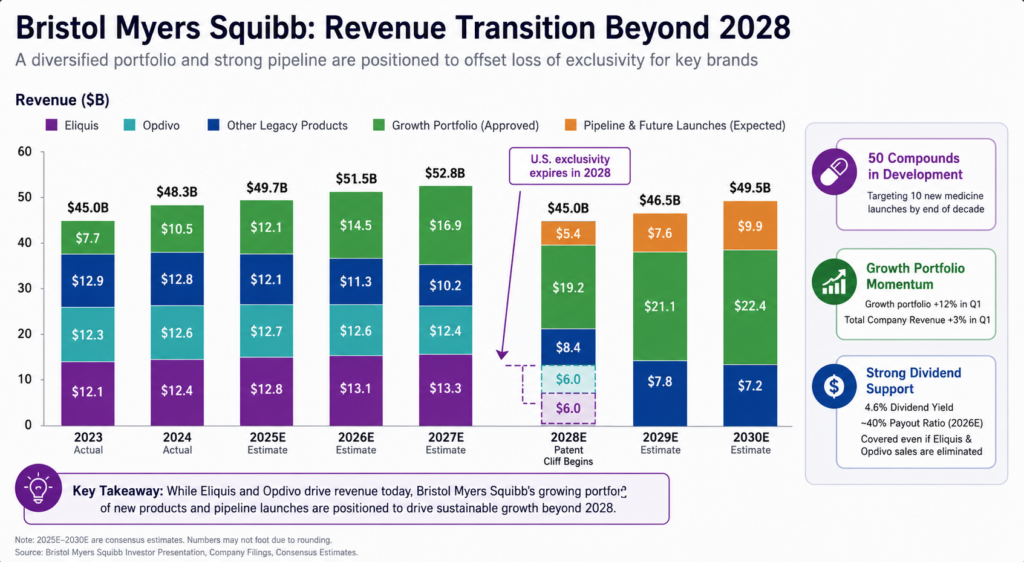

Just two drugs Eliquis and Opdivo generated more than $24.4 billion in sales last year, roughly half of the company’s total revenue. U.S. market exclusivity on both expires in 2028, after which lower-cost generic and biosimilar competition is expected to erode that revenue base.

Brokers from Eidellux walked through the company’s pipeline, balance sheet, and valuation to see whether the market’s skittishness has created an opportunity rather than a warning sign.

1. A revamped drug portfolio is ready to fill the gap

Pharmaceutical companies typically have years to prepare for patent expirations, and Bristol Myers Squibb has been proactively positioning itself for that challenge through both internal research and strategic acquisitions. The company currently has 50 drug candidates in development and aims to launch 10 new medicines before the end of the decade.

Among these programs, Cobenfy stands out as the most important pipeline asset. Already approved for schizophrenia, the drug could see substantial additional growth if it gains approval for Alzheimer’s disease-related psychosis. A crucial Phase 3 Adept-2 trial readout is expected later this year, making it a key catalyst for investors.

At the same time, Bristol Myers Squibb is collaborating with Johnson & Johnson on Milvexian, an experimental anticoagulant designed to treat atrial fibrillation and potentially offset future revenue declines from Eliquis. That program is also currently in Phase 3 clinical trials.

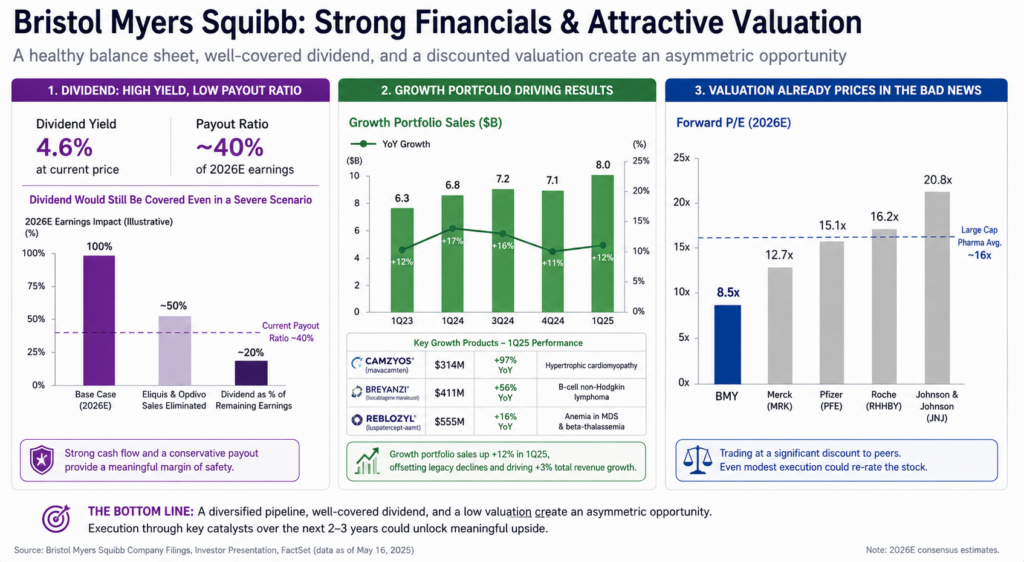

Beyond its pipeline, several recently launched products continue to deliver strong growth. In the first quarter, Camzyos sales increased 97% year over year to $314 million, Breyanzi grew 56% to $411 million, and Reblozyl rose 16% to $555 million. Overall, the company’s growth portfolio expanded 12% during the quarter, more than compensating for a 6% decline in legacy-product sales and helping drive 3% total company revenue growth.

While risks remain, particularly if Cobenfy’s Alzheimer’s-related trial results disappoint, the company appears to have multiple growth drivers already in place to help address the revenue challenges expected after 2028.

2. The 4.6% dividend looks well covered

Investors considering Bristol Myers Squibb do not need to wait for its pipeline to deliver results before seeing returns. The company currently offers a dividend yield of approximately 4.6%, and the payout appears well supported by earnings, representing only about 40% of projected 2026 earnings.

That relatively low payout ratio provides a significant margin of safety. Even in a severe scenario where sales from both Eliquis and Opdivo were eliminated, potentially reducing earnings by roughly half, the company could still have sufficient profits to support its dividend.

For income-oriented investors, the combination of a relatively high dividend yield and a conservative payout ratio is uncommon among large-cap pharmaceutical companies, making Bristol Myers Squibb an appealing option for those seeking both income and potential long-term value.

3. The valuation already prices in the bad news

Risk is part of this story, but valuation matters just as much as the risk itself. At a price-to-earnings ratio of 25, this stock would be far less attractive, since a setback in the pipeline would carry outsized downside relative to limited upside.

Instead, Bristol Myers Squibb trades at only 8.5 times its 2026 earnings estimate, a multiple that signals the market already expects very little growth from the company.

Valuation, in that sense, functions as a read on expectations: low multiples imply low expectations, which means even modest execution can move the stock. A scenario of mid-single-digit earnings growth through the patent cliff period looks sufficient to justify the current price. At the same time, the 4.6% dividend provides a meaningful floor under total returns even if the multiple never re-rates.

If Cobenfy’s Alzheimer’s program succeeds, that same depressed valuation could become the launchpad for substantial upside once sentiment catches up to the fundamentals.

Outlook

Bristol Myers Squibb is not without risk. The company’s 2028 patent cliff poses a significant, measurable challenge, and its long-term growth outlook depends heavily on the successful execution of its drug-development pipeline, which is far from guaranteed.

However, several factors support the investment case. Bristol Myers Squibb benefits from a diversified portfolio of newer, rapidly growing medicines, a dividend that is covered roughly twice by earnings, and a valuation that already appears to reflect a relatively cautious or pessimistic outlook.

Taken together, the stock looks more like an asymmetric opportunity than a traditional value trap. While investors must be willing to accept pipeline-related risks and potential volatility surrounding upcoming clinical milestones, the current share price may offer an attractive entry point for those prepared to hold through key catalysts over the next two to three years, given the range of potential outcomes still ahead.