The Federal Reserve’s preferred inflation measure drops on June 25, 2026, and it lands into one of the more constructively positioned market environments of the past several weeks. Micron just delivered its strongest quarter on record with a 24.31% EPS beat and Q4 guidance of $49 billion to $51 billion in revenue.

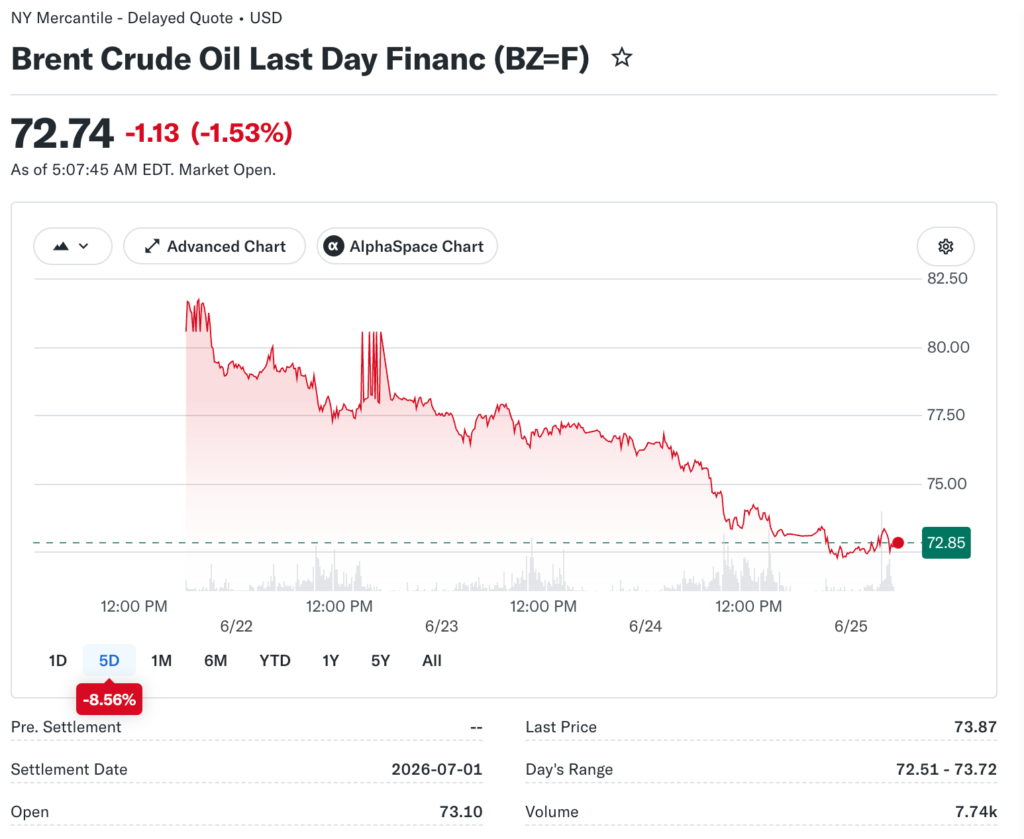

Brent crude settled at $73.74 per barrel on June 24, the lowest since before the Iran conflict began. The brand’s junior broker highlights why the May PCE print is the week’s final and most consequential data point, and what Winseterra sees as the most likely read for stocks across different outcome scenarios.

What PCE Consensus Is Projecting

Analysts heading into June 25 expect May PCE to come in at 4.1% year-over-year on the headline measure, up from April’s 3.8%. Core PCE, which strips out food and energy, is projected at 3.4% annually versus the prior 3.3%. Month-over-month, headline PCE is expected at 0.4% and core at 0.3%.

Those projections embed an important assumption. The energy cost relief from Brent crude falling from above $100 during the Iran conflict peak toward the low $70s may not yet be fully captured in the May reference period depending on the timing of price surveys.

If energy costs fell faster within May than the consensus estimate assumes, the actual PCE reading could come in below 4.1% and deliver a positive surprise for rate-hike probability across all sectors.

The Rate-Hike Probability That Hangs Over the Whole Week

Bank of America’s research note on June 23 outlined a scenario where the Federal Reserve hikes rates in September, October, and December of 2026. Before that note circulated, the probability of at least one hike by year-end sat at 50%, up from 24% in early April. The three-hike tail risk triggered selling in high-multiple technology stocks that had already partially priced the single-hike scenario.

A May PCE reading below 4.1% would immediately reduce the credibility of the three-hike scenario. It would signal that the Iran conflict’s energy contribution to inflation is unwinding faster than consensus assumed, giving the Fed room to hold through September without abandoning its 2% long-term target.

That outcome would likely trigger a rally in semiconductor stocks, homebuilders, and real estate investment trusts that have been under rate-hike pressure since the June 17 Fed decision.

What a Hot Print Would Do to the Micron Rally

The risk scenario for June 25 is a PCE reading at or above the 4.1% projection, combined with core PCE accelerating beyond 3.4%. That combination would validate the Bank of America rate hike scenario and introduce tension between the positive Micron earnings narrative and the negative rate-policy narrative.

Technology stocks can rally on strong earnings and sell off on rate fears within the same session, and a hot PCE print arriving while Micron’s after-hours gains are still fresh would test how much of the AI earnings enthusiasm is durable versus simply reactive.

Producer prices rose at 6.5% year-over-year in May, the fastest pace since November 2022, which signals that upstream inflation pressures were not resolving as quickly as headline energy prices would suggest. If those producer price increases flowed through to May PCE despite lower crude oil costs, the reading could surprise above the 4.1% estimate even as the energy component eases.

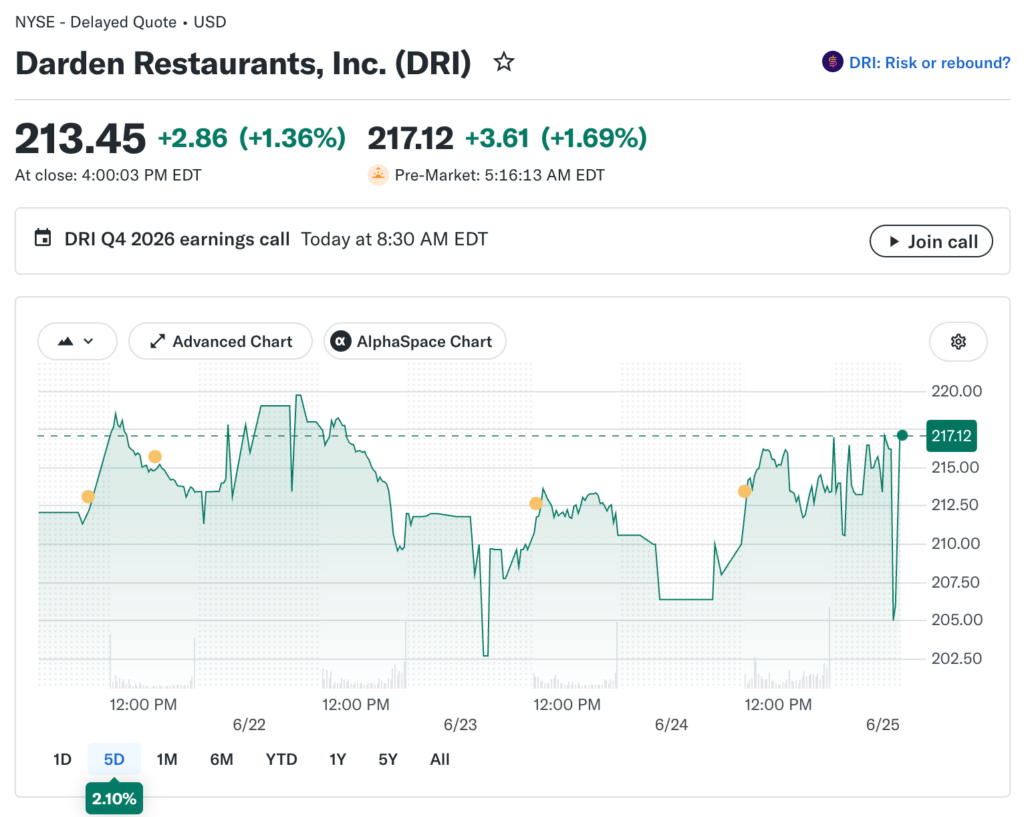

Q1 GDP and Darden as Supporting Data Points

June 25 also delivers the Q1 2026 GDP final estimate, with consensus expecting 1.4% annualized growth versus the prior reading of 1.6%. A final GDP figure below 1.4% would add a stagflationary flavor to any elevated PCE reading, creating the most uncomfortable combination for the Fed: sticky inflation alongside slowing growth.

Darden Restaurants reports Q4 fiscal 2026 earnings on June 25, adding a consumer spending data point to a day already dense with macro releases. Darden’s recent results showed same-restaurant sales growth of approximately 4.5% and total sales growth near 9.5% for fiscal 2026.

A constructive result from Darden would confirm that consumer spending on full-service dining remains intact despite elevated borrowing costs and inflation pressure.

Reading the Setup Into June 25 Trading

The combination of Micron’s historic earnings beat, Brent crude at $73.74, and a PCE print that may capture energy relief creates a constructively positioned market opening for June 25. The Dow finished June 24 at 51,848.90, up 0.35%, while the Nasdaq closed at 25,476.44, down 0.43%, ahead of the Micron report.

Investors tracking both the Micron 12.6% after-hours surge and the PCE release on June 25 morning should watch whether the two catalysts reinforce each other or create the kind of cross-current that keeps index performance flat while sector rotation accelerates beneath the surface.

The most important number on June 25 is whether the year-over-year PCE headline lands above or below 4.0%, the clearest binary outcome the market is positioned to trade around.