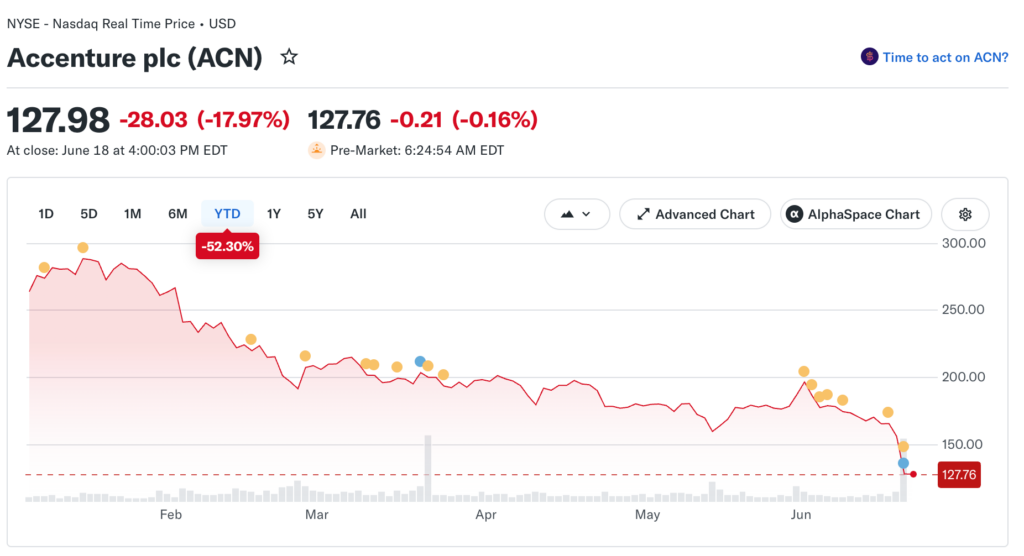

A quarter that beat on revenue and margins still triggered the steepest single-day drop in the company’s history, and the real story sits buried under the headline. Accenture’s fiscal Q3 2026 results read like a solid quarter on paper. Revenue landed at $18.7 billion, up 6% year over year. Adjusted earnings per share climbed 9% to $3.80.

Operating margin widened by 20 basis points to 17%, and free cash flow for the quarter came in at $3.6 billion. None of that stopped the stock from falling 17.97% on June 18, 2026, its worst single-day decline on record, erasing billions in value before New York had even reached lunch.

Brokers at Gammance argue the selloff has far less to do with the headline numbers than with what’s quietly showing up underneath them.

A Tiny Revenue Miss Wasn’t the Trigger

The actual revenue shortfall against consensus was somewhere between $60 million and $80 million, which works out to less than 0.4% of the quarter’s total revenue. A gap that small doesn’t typically send a large-cap stock down nearly 18% in a single session.

What actually moved the stock was a combination of three things landing together: softer forward guidance, a meaningful drop in new bookings, and a structural concern that management addressed head-on during the earnings call.

New bookings came in at $19.3 billion, down 2% year over year and roughly 13% below the record $22.1 billion booked the prior quarter. That sequential decline carries weight because bookings function as Accenture’s forward pipeline. They typically convert into recognized revenue over a window of 6 to 18 months, so a drop now signals weaker revenue later, and the market priced that delayed impact in immediately.

The Guidance Cut Did More Damage Than the Miss

Management trimmed the upper end of its full-year revenue growth outlook from 5% down to 4%. The midpoint of Q4 guidance landed about 2.3% below what analysts had expected. Accenture’s updated full-year forecast now calls for 3% to 4% growth in local currency, narrowed from a prior range of 2% to 5%.

Two specific pressures were named. Tensions tied to the Iran conflict pulled roughly $400 million out of quarterly revenue as clients delayed decisions. The second pressure is harder to put a number on but matters more for the long term: AI tools are starting to cut into demand for the kind of billable consulting hours that clients used to need, now that many of them are running AI systems internally.

Why the AI Concern Landed Differently This Time

Bloomberg Intelligence noted after the release that AI is reshaping demand patterns across consulting and managed services broadly, which lines up with what the market had already been pricing in before this report even landed.

Accenture shares had already dropped more than 50% from their 52-week high of $314.20 ahead of Thursday’s additional decline, meaning investors had been discounting this risk for months. The bookings drop simply gave that fear a concrete number to attach to.

The worry is fairly specific. A large share of Accenture’s business involves helping big companies design and integrate technology systems. If AI tools can now handle a growing portion of that integration work with fewer consultants involved, billable hours shrink along with it.

CEO Julie Sweet pushed back on the call, noting that clients still hit roadblocks scaling AI projects on their own and need experienced partners to get there. Analysts, judging by the stock reaction, weren’t fully convinced.

The Acquisitions Nobody Noticed

The same morning the earnings came out, Accenture announced three acquisitions worth roughly $4.18 billion combined, all aimed at the operational technology cybersecurity space. That market is valued near $27 billion in 2026 and is projected to grow to almost $59 billion by 2031, a roughly 16% annual growth rate. It’s also a segment where AI tends to support consulting work rather than replace it.

The market essentially shrugged. When bookings drop 13% from a record high and guidance gets cut on the same day, acquisition news tends to get ignored no matter how strategically sound it looks. Free cash flow guidance was actually raised, to a range of $10.8 billion to $11.5 billion from $9.8 billion to $10.5 billion previously, and that improvement went unrewarded too.

What Happens Next Will Matter More Than This Quarter

This report is the first real data point showing AI’s effect on enterprise consulting demand in hard numbers rather than analyst speculation. A 2% year-over-year bookings decline sounds minor. A 13% drop from a record quarter does not.

Anyone holding consulting or technology services stocks should treat this as an early signal rather than a one-off. Accenture’s next earnings report in September will show whether bookings stabilize or keep sliding, and that single number will likely tell investors more about the health of the entire consulting sector than anything analysts publish between now and then.