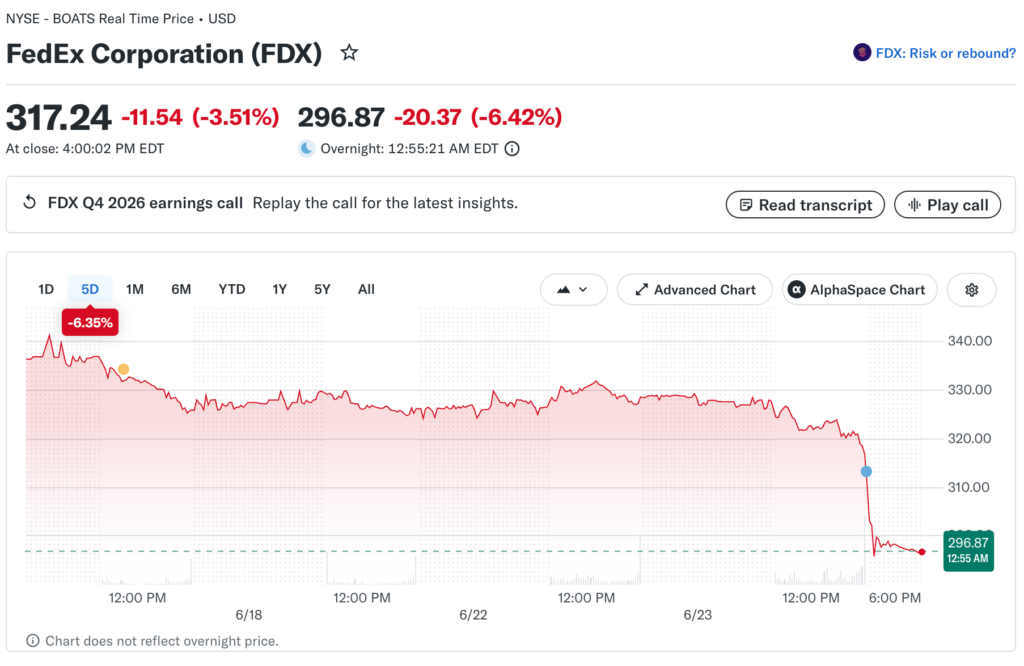

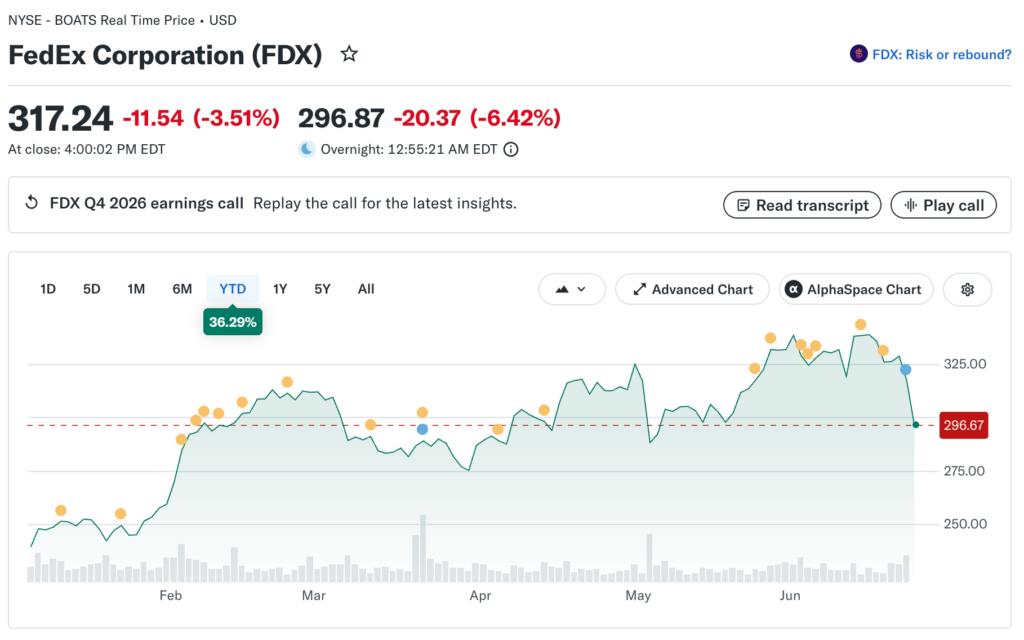

FedEx (FDX) reported fourth-quarter fiscal 2026 results on June 23, 2026, and the numbers delivered a cleaner story than the equity market’s chaotic session gave them credit for. Revenue rose to $25.0 billion, adjusted operating income came in at $2.09 billion, and capital spending as a percentage of revenue fell to 4.0%, the lowest annual rate in FedEx history.

The report also confirmed that the June 1 spinoff of FedEx Freight has been fully completed, making this the first earnings release from a structurally different company. A financial expert at Kepler-Group explores what the post-spinoff FedEx financials reveal about logistics demand, cost discipline, and the health of the US economy heading into the second half of 2026.

Revenue Growth That Outpaced the Prior Year by a Wide Margin

Q4 fiscal 2026 revenue of $25.0 billion compares to $22.2 billion in the same period of fiscal 2025, a $2.8 billion year-over-year increase driven by both volume growth and improved yield per package across the FedEx Express and Ground networks.

That revenue acceleration arrived in a quarter that included the tail end of the Iran conflict’s supply chain disruptions, which made international Express routing more expensive and time-consuming than normal.

Management introducing a calendar year 2026 outlook alongside traditional fiscal year results adds an unusual layer of transparency, signaling that the post-spinoff FedEx sees its near-term trajectory as positive despite the Fed’s hawkish rate posture.

The company expects continued revenue and earnings growth momentum in the June through December transition period, which is a constructive statement to make against a macro backdrop that has kept most management teams cautious.

The DRIVE Program’s Numbers Are Showing Up

FedEx’s DRIVE efficiency program, which targets billions in structural cost reduction through network consolidation and package handling automation, is the single most

important metric for investors evaluating whether the post-Freight-spinoff FedEx story has fundamental legs. Capital spending falling to 4.0% of revenue is the most direct evidence yet that DRIVE is delivering on its promises at the pace management originally targeted.

FedEx’s capital spending had been running significantly higher in prior years as the company invested in network integration. The compression to the lowest level in company history while revenue grew by $2.8 billion year-over-year is precisely the operating leverage the FDX bull case has been built on.

Adjusted operating income of $2.09 billion compares to $2.02 billion in the prior year, a directionally positive move against a comparison period that included a more complete legacy cost structure.

What the Iran Conflict Cost FedEx and What Recovery Looks Like

International air freight volumes were meaningfully disrupted throughout the Iran conflict period, which ran from late 2025 through the ceasefire framework signed in mid-June 2026. FedEx Express routes through the Middle East and Central Asia were rerouted or reduced, adding measurable cost and extending delivery times for customers moving goods through those corridors at the conflict’s peak.

The ceasefire framework, which includes reopening the Strait of Hormuz, directly benefits FedEx Express by restoring more direct routing options for international shipments.

Management’s introduction of a full calendar year 2026 outlook implicitly assumes the ceasefire holds and that route normalization allows Express margins to recover toward pre-conflict levels through the second half. Any acceleration in that margin recovery timeline would represent upside to current analyst models.

Reading FedEx as an Economic Indicator

Logistics companies are among the most reliable leading indicators of economic activity because they measure actual goods movement rather than surveys or sentiment. FedEx’s Q4 revenue growth of 12.6% year-over-year was not driven by pricing alone.

Volume grew across both Express and Ground networks, reflecting genuine economic demand that directly contradicts any thesis that consumer and business spending is collapsing under elevated interest rates.

That signal carries implications beyond FDX shareholders. Consumer discretionary companies, industrial manufacturers, and retailers all depend on the same freight infrastructure that FedEx operates.

When that infrastructure is growing revenue at double-digit rates while simultaneously reducing capital intensity, it tells you something constructive about the demand environment that was not reflected in the June 23 technology-dominated session.

The Calendar Year Transition and What Analysts Will Focus On

FedEx’s fiscal year change from a May 31 year-end to a December 31 year-end became effective June 1, 2026. That transition creates a six-month reporting period running June through December 2026, which management has introduced its first calendar year outlook to address explicitly.

Analysts will focus on whether the revenue and margin trajectory in that transition period confirms or challenges the post-DRIVE efficiency thesis heading into the company’s first full calendar year as a pure-play parcel and logistics business.

The lowest capital spending percentage in company history, combined with revenue growth and improving margins, provides a strong foundation for that first calendar year guidance. Investors watching FDX should treat the company’s results as a stabilizing fundamental signal in a week that otherwise delivered volatility-amplifying macro news at almost every turn.