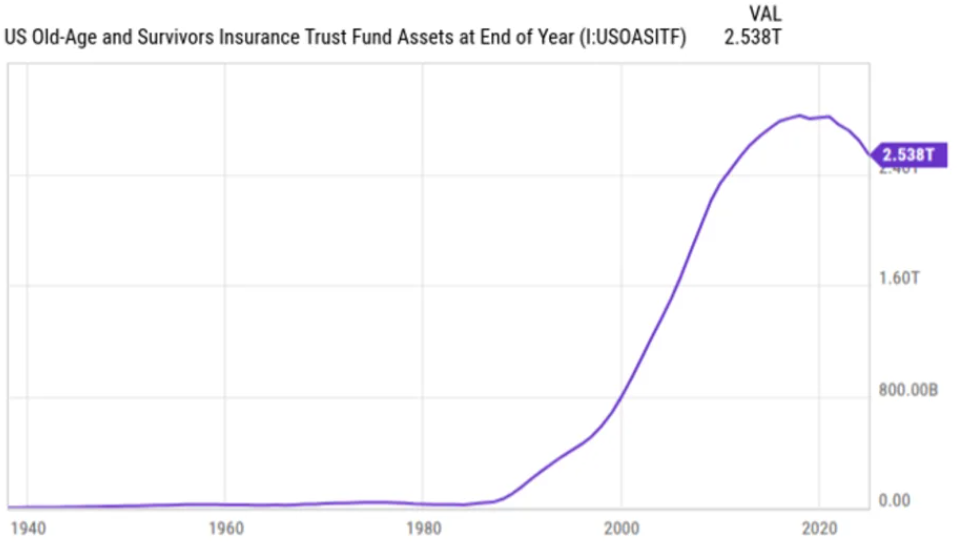

Workers currently in their 50s and 60s may face a retirement landscape that looks very different from what they originally expected. The Social Security Old-Age and Survivors Insurance (OASI) Trust Fund is now paying out more in benefits each year than it receives through payroll taxes and interest income, and the funding shortfall is growing faster than previously projected.

According to Fondesia‘s specialists, understanding the latest funding forecasts is becoming increasingly important for anyone planning to claim Social Security benefits within the next decade, as future funding pressures could influence long-term retirement planning and benefit expectations.

Depletion date moves up to late 2032

According to the latest Social Security Trustees Report, the Old-Age and Survivors Insurance (OASI) Trust Fund is now projected to deplete its reserves before the end of 2032, several months earlier than the previous forecast, which anticipated depletion in early 2033.

If no legislative changes are made before then, the program would be able to pay only about 78% of scheduled benefits using incoming payroll tax revenue alone, with that percentage projected to decline further over time under current actuarial estimates.

This updated timeline is significant because it shortens the planning horizon for workers approaching retirement. For example, someone who is 55 years old today will be around 62, the earliest Social Security claiming age, when the trust fund is expected to face funding shortfalls, placing them directly within the critical decision-making period for retirement benefit claims.

Why claiming early to “beat the cuts” can backfire

Faced with the prospect of a 22% (or larger) benefit reduction down the line, some near-retirees may be tempted to claim as early as possible, reasoning that 100% of a smaller check now beats 78% of a larger one later. Fondesia’s analysis suggests this logic breaks down under closer scrutiny.

Claiming before full retirement age already locks in a permanent reduction of often 25–30% below the full benefit, depending on birth year. Stack a future across-the-board cut of up to 22% on top of that, and an early claimant ends up absorbing both penalties simultaneously over the course of retirement, rather than just one.

There is another important consideration for early claimants. Individuals who begin collecting Social Security benefits before reaching full retirement age while continuing to work may be subject to the retirement earnings test, which can temporarily reduce benefits if earnings exceed certain annual limits. In addition, a portion of their Social Security income may become subject to federal taxation, depending on overall income levels.

For many workers, delaying benefits remains the more financially advantageous option. By postponing claims beyond full retirement age, retirees can earn delayed retirement credits that increase benefits by approximately 8% per year, with these enhancements continuing to accumulate until age 70, resulting in significantly higher lifetime payouts

Delaying still looks like the stronger play for most

For the bulk of near-retirees, Fondesia’s view is that the most effective response to this report is no change at all to an existing claiming strategy. Social Security functions as longevity insurance protection against outliving savings, and that function is strongest when claimed later rather than earlier.

The core strategic principle holds: waiting well past age 62, and ideally toward full retirement age or beyond, is generally what produces the strongest income floor for the 80s and 90s, the years when retirees are most exposed to running short of other assets.

Congress has a track record of acting at the last minute

There’s also a political variable worth weighing. Lawmakers have the authority to shore up the trust fund through tax adjustments, benefit formula changes, or other reforms — and history suggests they tend to wait until the deadline is nearly on top of them before acting. That’s precisely what happened in the 1980s, the last time the program approached insolvency, when a last-minute legislative fix preserved benefits before the fund actually ran dry.

Based on that precedent, Fondesia’s base case is that near-retirees are unlikely to see a benefit cut anywhere close to the full 22% currently projected — and there’s a reasonable chance no cut materializes at all if Congress intervenes before 2032.

Outlook: stay the course, but watch the calendar

The most likely scenario between now and 2032 is a period of continued political and legislative deadlock, followed by a last-minute policy solution, mirroring how previous Social Security funding challenges have been addressed.

For workers approaching retirement age, the report should serve as a reason to reassess retirement plans not abandon them. Key areas to review include:

- The benefits of delaying Social Security claims to maximize delayed retirement credits.

- Potential earnings test implications for those who plan to continue working while receiving benefits.

- The impact of a potential 15%–25% reduction in benefits under a worst-case scenario on overall retirement income needs.

Unless there is a major legislative overhaul, a delayed-claiming strategy remains one of the most resilient approaches for maximizing lifetime benefits and maintaining retirement income security beyond 2032.