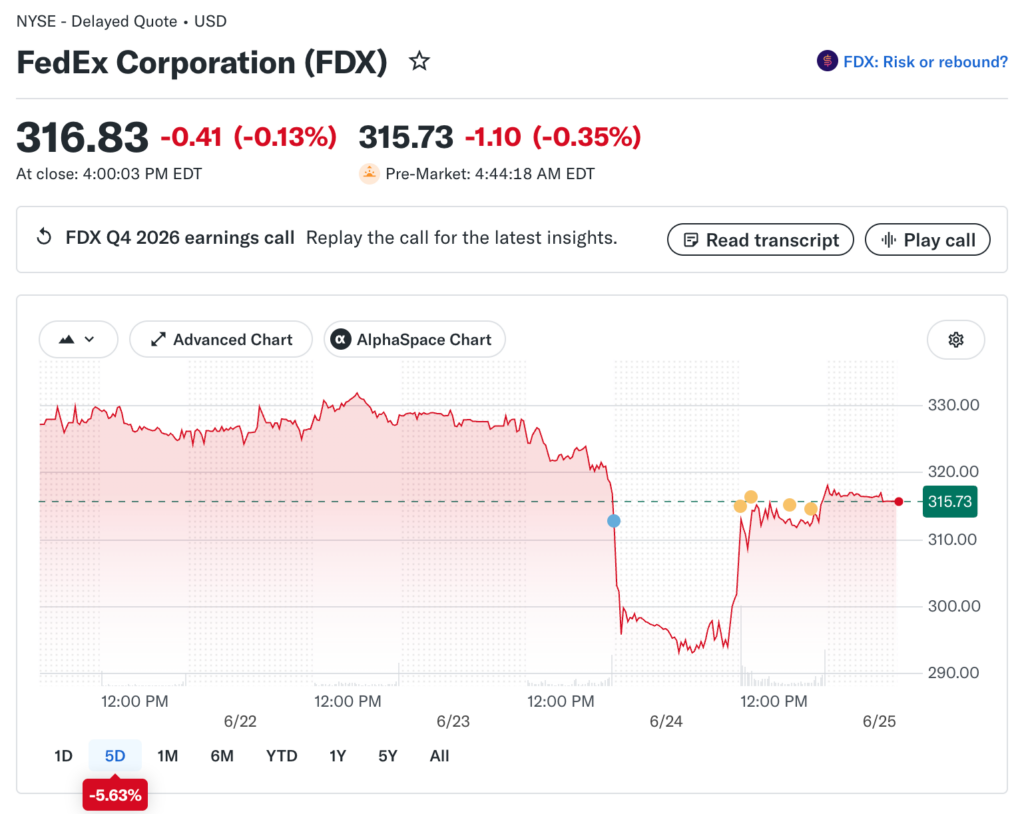

Strong quarterly results should push a stock higher. FedEx delivered exactly that on June 23, 2026, posting fourth-quarter revenue of $25 billion against a $24 billion expectation and earnings per share of $6.31 versus the $5.96 Wall Street had penciled in. The stock then fell roughly 7% in premarket trading the following morning and had already dropped around 6% in after-hours the night of the report.

A financial analyst at Winseterra takes a closer look at why the FedEx reaction is one of the more instructive paradoxes this earnings season has produced, and what the underlying numbers actually say about a business most investors stopped reading carefully once the share price ran 75% over the prior year.

When the Price Already Said Everything

A stock advancing 75% in twelve months does not arrive at its earnings release with a blank slate. Every percentage point of that gain represents investor capital that placed a bet on what the company would deliver.

When the delivery matches or modestly exceeds a high-confidence expectation, there is no remaining buyer who has not already acted. The seller waiting for confirmation has their confirmation, and the buyer who needed the numbers before committing already paid up months earlier.

That dynamic explains the FedEx reaction more precisely than any operational disappointment would.

Citi analysts described the after-hours decline as largely unjustified, noting that high expectations, FedEx’s strong prior-year advance, and the lack of comprehensive standalone financials probably explained the drop. That phrasing separates what the business delivered from how the market chose to respond to it.

The Freight Spinoff Creates a Reporting Gap

This was the final earnings report to include FedEx Freight, which completed its separation as an independent publicly traded company on June 1.

That structural change creates a comparison problem that investors are still adjusting to. Revenue that existed in the Q4 fiscal 2026 total will simply disappear from the Q1 fiscal 2027 report, not because business deteriorated but because a division changed its ownership structure and will now report separately.

That kind of reporting discontinuity generates uncertainty, and markets price uncertainty with a discount even when fundamentals are intact. Investors who have not yet rebuilt a clean model for the standalone FedEx, excluding Freight from historical periods, are working with incomplete information. The after-hours selling reflected that informational gap as much as any concern about the operational quarter itself.

What $25 Billion in Revenue Actually Represents

Pulling back from the stock reaction and looking at the numbers alone, FedEx moved $25 billion in logistics revenue in a single quarter. That compares to $22.2 billion in the same period a year earlier, a year-over-year increase of $2.8 billion.

That growth arrived in a quarter still carrying the rerouting costs and route disruption from the Iran conflict on international Express operations. Growing revenue at 12.6% year-over-year while absorbing those geopolitical costs is not a weak result by any historical standard.

Capital spending as a percentage of revenue fell to the lowest annual level in company history, which is the most direct evidence yet that the DRIVE efficiency program is compressing costs at the pace management originally targeted. For a company building its investment thesis around margin expansion rather than simple revenue growth, hitting the lowest capex intensity in company history during a quarter of strong volume is precisely the data point the bull case needed to confirm.

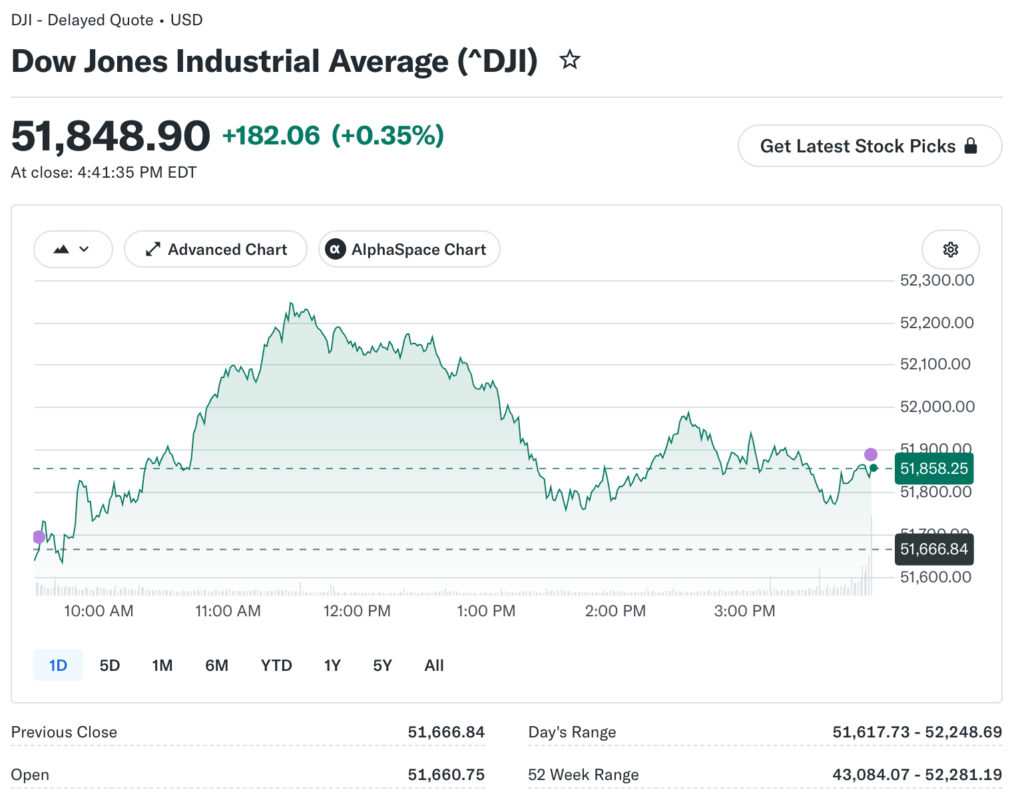

Alphabet Joins the Dow on the Same Day

While FedEx dominated the June 24 premarket conversation, S&P Global announced that Alphabet would replace Verizon in the Dow Jones Industrial Average.

Alphabet responded by closing down 0.2% on the day the news broke, which runs counter to the intuition that Dow inclusion creates demand from passive tracking funds. The muted reaction reflects the broader AI cost concern narrative that had been weighing on Alphabet since the Bank of America rate note circulated on June 23.

The Dow has been outperforming the Nasdaq since the June 17 Fed decision partly because its lower technology concentration provides a buffer when AI cost concerns reprice high-multiple names. Adding Alphabet narrows that buffer, which means the Dow’s behavior as a defensive benchmark during technology selloffs will look different once tracking funds complete their rebalancing.

Reading the Result Before the Next Report

FedEx’s next earnings release, the first to cover a full quarter as a standalone parcel and logistics company without Freight in the comparison period, will be the real test of whether the post-spinoff investment thesis is generating the returns management promised.

The operational momentum in the June 23 results, including the revenue beat, the earnings beat, and the record-low capex ratio, provides a strong starting point for that first clean standalone quarter.

Investors who sold the post-earnings dip based on the stock reaction rather than the business result may find themselves revisiting that decision when Q1 fiscal 2027 numbers arrive without the Freight comparison complexity clouding the analysis.