Qualcomm (QCOM) has spent years known mainly as a premium smartphone chipmaker living off the mobile boom. Yesterday’s investor day suggests that identity is starting to shift. Risance‘s equity research team breaks down what the company unveiled and why the market reacted the way it did.

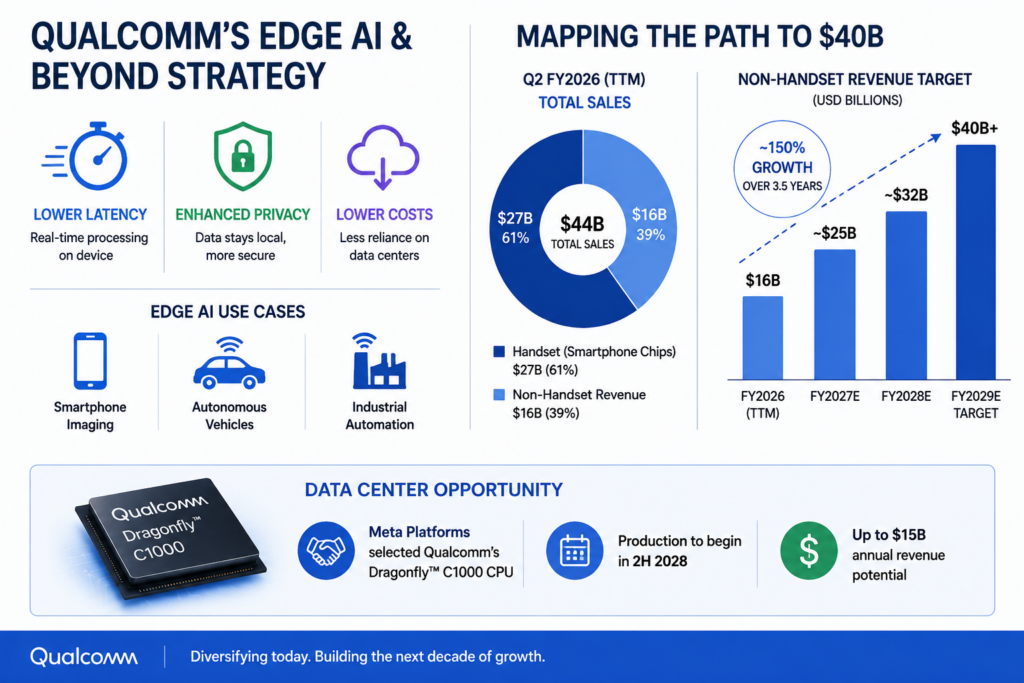

Qualcomm laid out plans to more than double its non-handset revenue to $40 billion within three years, alongside a combined total addressable market estimate of $1.7 trillion by 2030. The headline revenue growth itself isn’t the real story. What matters is the shift in where that revenue comes from, with AI compute positioned as the primary driver behind several large new markets the company is now chasing.

Shares jumped 11% in premarket trading and, even after some of that initial enthusiasm faded, were still up roughly 8.5% by early afternoon. For investors willing to hold over a three-to-five-year horizon, the more interesting question is whether Qualcomm can actually capture the opportunity it just described.

A Pivot Investors Have Been Waiting For

Qualcomm’s manufacturing expertise in smartphone chips puts it in a strong position to chase a market that hasn’t fully taken off yet: edge AI compute. Most AI models today run in data centers, which is exactly why cloud infrastructure spending has exploded. Running AI directly on the device itself, whether a phone, a car, or an enterprise sensor, remains a largely untapped opportunity.

Qualcomm’s leadership is betting that AI models will keep getting more efficient at inference, the stage where a trained model actually produces an output, while leaner, task-specific models built for narrower jobs become viable to run locally rather than in the cloud.

Why On-Device AI Is Becoming Unavoidable

As AI models become more powerful and general-purpose, they are not always the best fit for specialized, real-time, or privacy-sensitive applications. This is where edge AI becomes increasingly valuable.

By processing data directly on devices rather than relying on distant cloud servers, edge AI significantly reduces latency, which is critical for applications such as smartphone image processing, autonomous vehicles, and other time-sensitive systems where instant responses are essential.

Beyond speed, on-device AI enhances privacy by keeping sensitive data local and can help businesses reduce reliance on expensive data center infrastructure, making it an increasingly attractive solution as AI adoption continues to expand.

Mapping the Path to $40 Billion

The numbers behind Qualcomm’s target are worth examining closely. As of the second quarter of fiscal 2026, ended March 29, the company’s trailing twelve-month sales totaled $44 billion, with non-handset revenue contributing just over $16 billion and the remaining $27 billion still coming from smartphone chips.

Hitting the $40 billion non-handset goal means growing that segment by roughly 150% over the next three and a half years, with edge computing expected to supply more than a third of that growth.

Qualcomm also sees its push into data centers contributing as much as $15 billion annually. Meta Platforms has already agreed to use Qualcomm’s new data center CPU, the Dragonfly C1000, to power its next-generation infrastructure, with production expected to begin in the second half of 2028.

A Cheap Stock for a Business About to Change

Today’s rally reflects investor confidence in Qualcomm’s broader ambitions beyond the smartphone cycle, which has been a real drag on the stock historically. Handset upgrade cycles run three to four years rather than annually, leading to uneven demand for legacy chips.

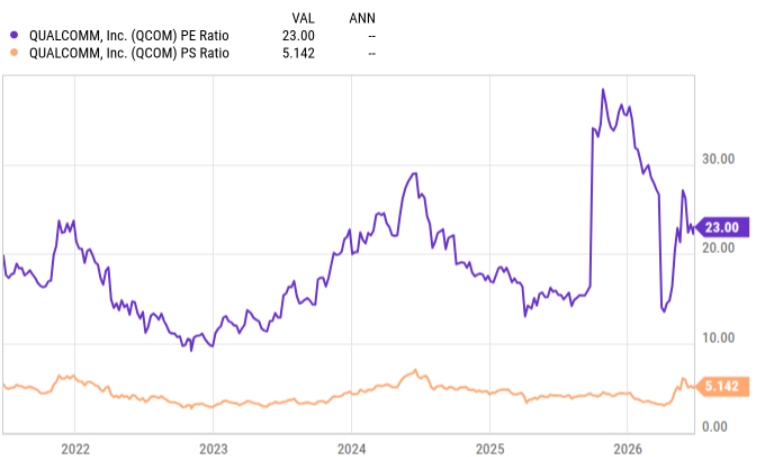

Over the past five years, Qualcomm shares have gained just 57%, trailing both the Nasdaq-100 and the S&P 500 by a wide margin.

That underperformance has left the stock trading at a little over 23 times trailing earnings and around 5 times sales, levels that look inexpensive for a company positioning itself inside the AI infrastructure buildout that’s commanding premium multiples elsewhere in the market.

The Real Test: Can Qualcomm Actually Win Share

Qualcomm’s opportunity in AI and data-center chips is significant, but capturing market share will be far more challenging than identifying the market itself. Major cloud providers are focused on obtaining the best-performing chips at the lowest cost, while companies such as Alphabet and Amazon are increasingly developing custom in-house silicon rather than relying on third-party suppliers.

For investors, the key question is not whether the market opportunity exists—it clearly does. The challenge is whether Qualcomm can successfully compete against well-funded rivals and hyperscalers that are building their own chip ecosystems.

Moving beyond its traditional smartphone-focused business presents meaningful execution risk, but it is also an important strategic transition. If Qualcomm can establish itself in AI infrastructure and adjacent markets, the company’s growth profile over the next decade could look very different from the one that defined its past success.

.