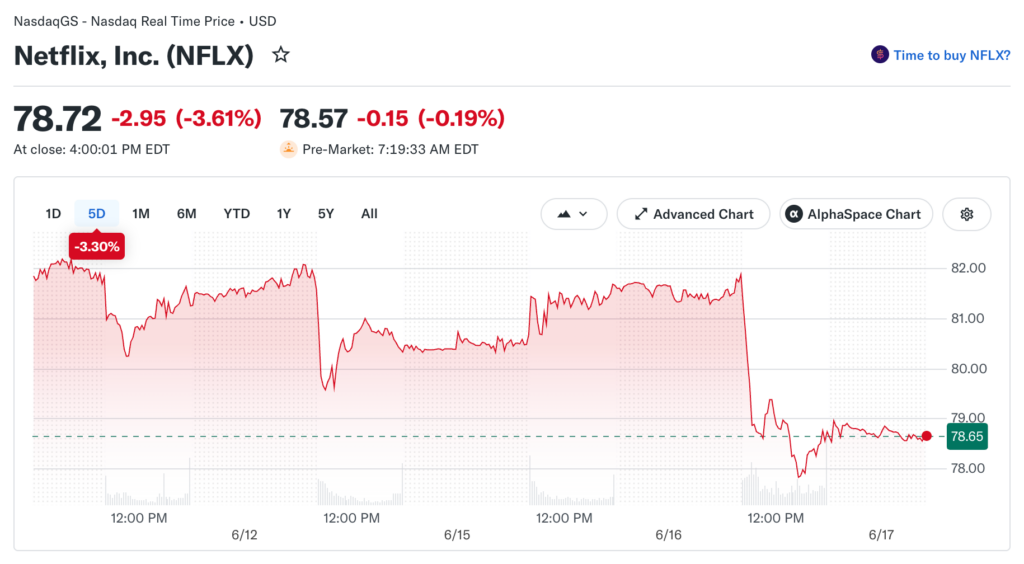

Netflix (NFLX) fell 3.68% on June 16, 2026, closing near $78.72 and landing roughly 39% below its all-time high, even as the broader market posted mixed results following the US-Iran ceasefire news.

The stock’s failure to join the relief rally that lifted tech names broadly on June 15 isn’t random. Risance‘s lead financial analyst walks through what’s actually driving the decline, and why it’s a different story than the one weighing on other large-cap tech names right now.

A Selloff That Doesn’t Match the Tape

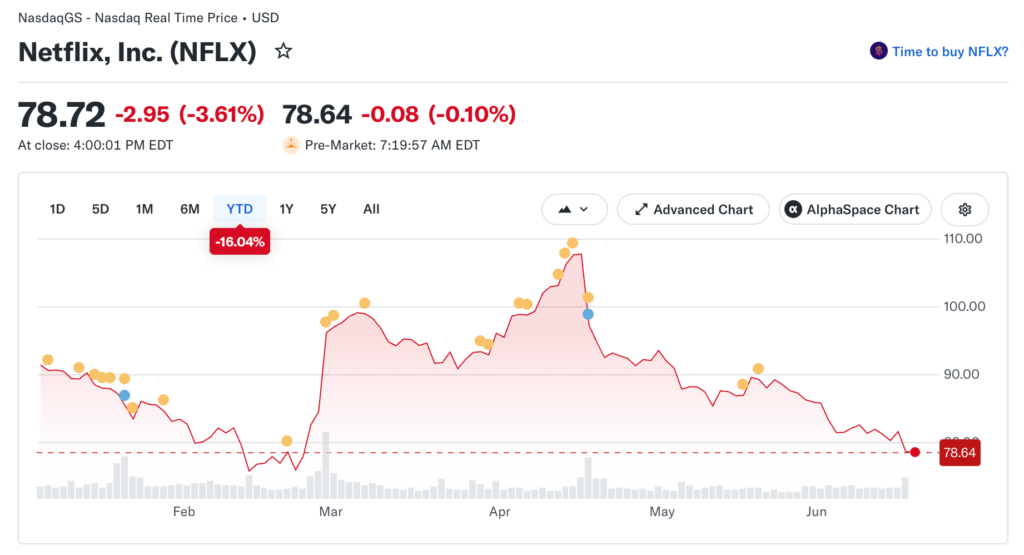

Netflix’s slide from its all-time high has picked up speed since the April 2026 earnings report. The stock has fallen 25% since that release while the S&P 500 gained 4% over the same stretch, a gap that has nothing to do with subscriber losses or weakness in the company’s core numbers.

Q1 revenue came in at $12.25 billion, beating the $12.18 billion consensus, while net income hit $5.28 billion, more than double the $2.42 billion reported the prior quarter. The real driver is structural, not operational: 10-year Treasury yields sitting near 96th-percentile highs create a discount-rate problem that strong quarterly numbers alone can’t offset for a long-duration growth stock like Netflix.

When the rate used to discount future cash flows climbs sharply, present value falls even if the business is performing exactly as expected. Netflix draws most of its valuation from earnings projected years out, which makes it considerably more sensitive to this dynamic than companies trading on near-term earnings multiples.

Why Advertising Revenue Is the New Scoreboard

Netflix has stopped reporting quarterly subscriber additions, removing the metric investors once used to gauge platform health. In its place, advertising revenue has become the key forward-looking growth signal, with analysts projecting it will reach $3 billion in 2026 as the ad-supported tier continues scaling globally.

Live Programming Raises the Stakes on Margins

On June 16, Netflix expanded its exclusive partnership with iHeartMedia to roll out celebrity-focused video podcasts and live broadcasts, adding a new content category alongside real execution risk.

Live and creator-led unscripted programming typically carries higher production and talent costs than scripted content, and if the new formats don’t drive engagement gains proportional to that spend, they could squeeze Netflix’s current 28.5% net income margin without delivering the advertising lift the strategy is banking on.

Full-year 2026 operating margins are projected at 31.5%, and Q1 results tracked in line with that path. The open question is whether the live-content pivot can hold that margin as the cost base shifts toward higher variable-cost programming at scale.

What Insiders and Prediction Markets Are Signaling

Analysts have also flagged growing reliance on price increases rather than organic subscriber growth as the main lever behind recent revenue gains. Insiders have net-sold across 107 recent transactions, suggesting limited internal conviction that shares are undervalued at current levels.

Prediction markets currently assign just 12% odds of NFLX reaching $90 by the end of June, implying little expectation of a near-term catalyst large enough to drive a meaningful recovery from current levels near $78. The next scheduled earnings date, July 16, 2026, is the point where both analyst estimates and prediction-market odds are likely to reset in a meaningful way.

What It Would Take for the Bull Case to Work

Wall Street’s average price target sits at $114 per share, well above the current trading range. Seaport Research’s Mahaney maintains a Buy rating, pointing to ad-tier growth and international expansion as underappreciated drivers, and Jefferies holds a similarly constructive view on the stock’s 12-month outlook.

For that bull case to play out, two things need to happen at once: 10-year yields need to retreat from near-record levels as the Fed signals an eventual path toward easing, and advertising revenue needs to visibly accelerate in the Q2 report rather than remaining a forward-looking projection disconnected from what’s actually being reported.

If yields stay elevated following the Fed’s June 17 decision, the discount-rate problem doesn’t go away no matter how well the business executes quarter to quarter.

The Countdown to July 16

Netflix delivered a strong Q1 earnings beat, reporting EPS of $1.23 versus the $0.76 consensus estimate, a 61.21% positive surprise. Under normal market conditions, such a result would likely have supported a meaningful rally in the stock.

However, Netflix shares continued to decline, highlighting how rising interest rates and broader market conditions are currently having a greater influence on valuation than company fundamentals.

Looking ahead to July 16, investors should pay close attention to the 10-year Treasury yield, particularly the 4.5% level, alongside Netflix’s own revenue and engagement metrics. A sustained recovery in the stock may require both improving company performance and a more favorable interest-rate environment.