Something shifted in how the market entered June 25, 2026. Micron reported the strongest quarter in its history after the close on June 24, clearing a revenue target of roughly $35 billion and landing closer to $41.46 billion while guiding Q4 to between $49 billion and $51 billion.

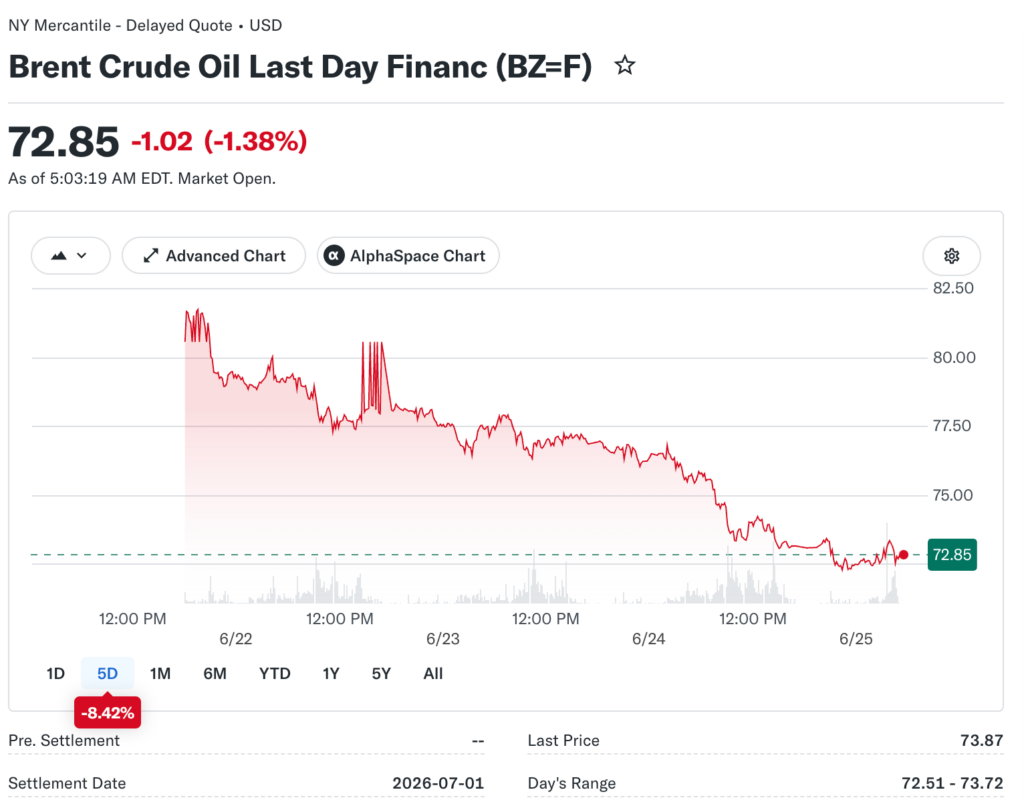

Brent crude had already slid to $73.74 per barrel, its quietest settlement since the Iran conflict first pushed oil above $100 back in late February. The brand’s senior financial advisor mentions that Winseterra sees June 25 as the point where several separate narratives either arrive at a shared conclusion or stay in tension heading into the weekend trading gap.

What Crude Oil Near $73 Does to the Inflation Calculation

The retreat in Brent from above $100 during peak conflict conditions to $73.74 on June 24 carries direct implications for how the May PCE print will read when it arrives on June 25 morning.

Earlier research from the Federal Reserve Bank of Dallas concluded that the Iran war’s energy disruption added roughly 1.7 annualized percentage points to headline PCE during the first quarter of 2026. That was not a rounding error. It was a conflict-driven spike that the central bank could not realistically address with rate hikes without simultaneously tightening into a supply-shock environment.

The distinction investors are tracking on June 25 is whether the oil retreat shows up in May PCE as a deceleration or an active monthly reversal. A deceleration gives the Fed reason to pause. An active reversal pushes the first hike timeline from a Q3 certainty into a Q4 possibility, a material shift for any long-duration equity that reprices when discount rate assumptions change.

The Index That Told the Honest Story on June 24

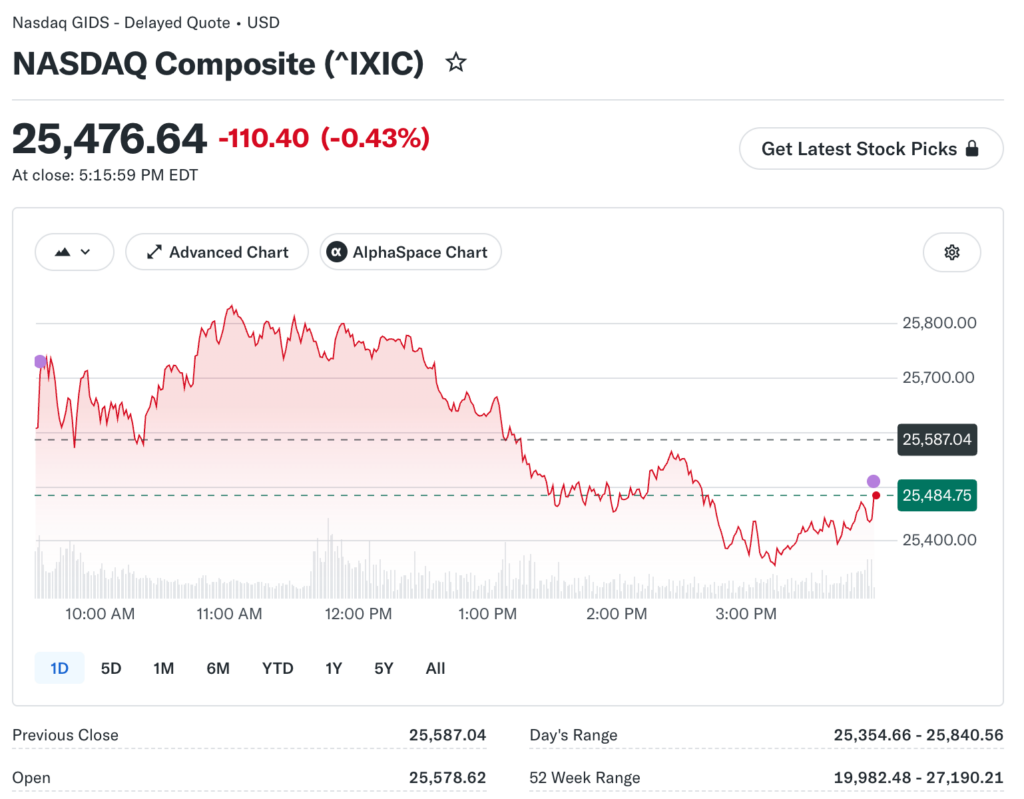

The Nasdaq closed June 24 at 25,476.44, down 0.43%, while the Dow added 182.06 points to finish at 51,848.90 and the Russell 2000 gained 0.37% to close at 2,986.63. That three-way split, two indices gaining while the primary technology benchmark fell, captures something more useful than any single headline number from the session.

The Dow’s industrial and financial composition makes it less sensitive to discount rate anxiety than the Nasdaq’s technology-heavy mix. The Russell 2000’s advance on a day when rate-hike fear was present tells you small-cap investors are weighing lower oil input costs more heavily than potential rate increases.

Both signals suggest the broader economy is absorbing the Fed’s hawkish posture without the demand collapse that more aggressive rate-hike scenarios would predict.

Alphabet Enters the Dow at an Awkward Moment

S&P Global confirmed on June 24 that Alphabet will replace Verizon in the Dow Jones Industrial Average. The announcement arrived while Alphabet shares were already under pressure from the AI cost concern narrative that Bank of America’s rate note sparked on June 23, and the stock closed down 0.2% on the day of the news.

Under ordinary circumstances, Dow inclusion generates visible demand from passive index funds that must buy shares to match the new composition.

The muted response reflects how thoroughly macro narrative was overriding index mechanics on June 24. Once that pressure eases, through a soft PCE reading or Micron’s earnings normalizing AI infrastructure sentiment, the passive rebalancing demand for Alphabet will arrive on schedule. It simply landed during a session where it could not be seen through the noise.

KB Home’s Number and What It Represents

KB Home gained roughly 3% on June 24 after reporting fiscal second-quarter revenue of $1.11 billion against a $1.10 billion estimate. That narrow beat carries more analytical weight than the size of either number suggests. The thirty-year fixed mortgage rate has been running near 6.47% throughout this quarter. At that financing cost, a buyer adding a new home absorbs a payment burden meaningfully higher than anything seen in the decade before 2022.

A homebuilder posting revenue above estimates in that environment is not confirming that the housing market has recovered. It is confirming that demand has not buckled under conditions the most pessimistic rate models said would be fatal to new home sales. That signal places a floor beneath the consumer demand story rather than confirming a ceiling above it.

The Threshold That Defines the June 25 Session

Micron’s historical earnings result, Brent crude below $74, constructive consumer data from Victoria’s Secret, KB Home, and Darden, and a Dow and Russell 2000 that held their gains even while the Nasdaq was cautious, these factors collectively present the most supportive market backdrop since the June 17 Federal Reserve decision reset rate expectations higher.

May PCE arriving on June 25 morning holds the power to amplify everything built across the prior four sessions or neutralize it in a single data release. A year-over-year headline reading below the 4.1% consensus estimate, even modestly, validates the thesis that the conflict’s energy inflation contribution is unwinding in real time.

A surprise above that threshold hands rate-hike advocates their argument and asks the equity market to decide how much of Micron’s after-hours enthusiasm survives a tighter monetary outlook.