US banking stocks advanced on June 25 after the Federal Reserve confirmed that major lenders had passed its annual stress test, clearing the regulatory path for dividend increases across the sector. The stress test results arrived alongside Micron’s earnings surge,

May PCE data, and a Dow Jones Industrial Average closing at a new all-time record, which meant the bank sector news received less attention than its actual significance for income investors and financial sector holders warranted.

Kepler Group’s expert broker shares what the stress test clearance tells investors about bank capital health, dividend growth potential, and the financial sector’s position in the current rate environment heading into the second half of 2026.

What Stress Tests Actually Measure

The Federal Reserve’s annual bank stress tests run major lenders through hypothetical severe economic scenarios to assess whether their capital buffers can absorb significant losses without threatening broader system stability. Passing the test does not simply mean the bank survived the simulation.

It means regulators are satisfied that the bank can maintain adequate capital ratios even under conditions significantly worse than the current economic environment, and banks that fail or come close to failing face restrictions on capital return that can last well into the following year.

For investors, the stress test clearance matters primarily because it unlocks the ability to return capital at scale. Banks that pass can increase dividends and expand share buyback programs without regulatory restriction, creating direct and measurable cash returns for shareholders that are independent of broader market direction or AI sentiment.

The Rate Environment Works in the Banks’ Favor

Banks earn profit from the spread between what they pay depositors and what they charge borrowers. When short-term rates stay elevated, as they have since the Fed’s June 17 hold at 3.50 percent to 3.75 percent, that spread widens for most lenders relative to the near-zero rate environment of 2020 and 2021.

Higher rates mean higher net interest income per loan dollar outstanding, and that improvement flows directly to the bottom line without requiring additional loan growth.

The June 25 PCE data showing inflation at 4.1 percent annually, combined with the GDP revision to 2.1 percent growth and stable jobless claims at 225,000, reduces the probability of imminent rate cuts to near zero.

For bank stocks, that is the most favorable possible rate backdrop available in the current macro environment. A Fed that is not cutting rates is actively preserving the net interest margin environment that has been supporting bank earnings growth throughout 2026.

Dividend Growth as the Core Investment Thesis

Stress test clearance enables banks to raise their dividends, and that announcement coming on a day of uncertain equity market direction gives financial stocks a specific, tangible catalyst that does not depend on AI sentiment or the inflation trajectory. A dividend increase is a direct and predictable cash return regardless of what the market does with the stock price in subsequent sessions.

Major bank dividend increases following stress test clearance tend to attract institutional capital from income-oriented funds that were underweight financials during the period of rate uncertainty. That reallocation creates demand for bank stocks independent of any fundamental change in the lending business itself, adding mechanical support beneath the stock prices of the largest dividend-raising banks.

How Banks Fit the Broader June 25 Market Story

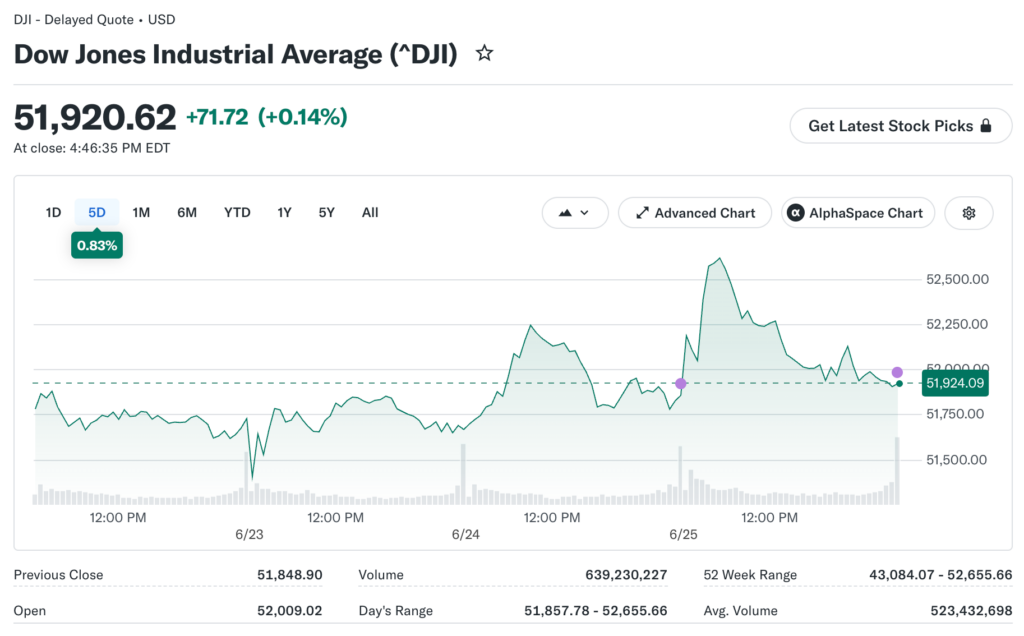

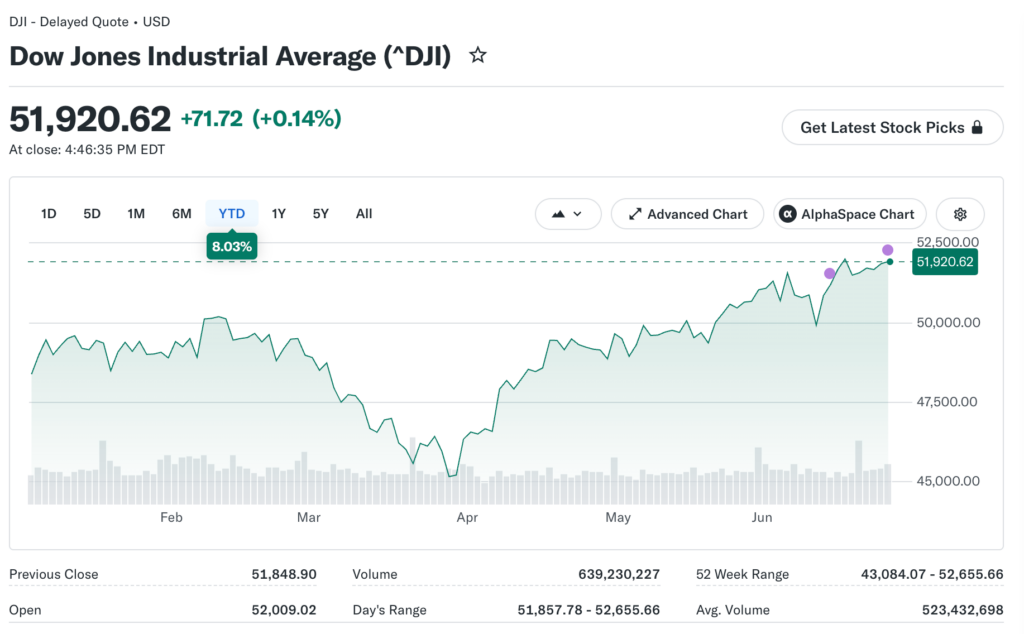

The Dow Jones Industrial Average hit a new record near 52,500 on June 25, driven by industrials, financials, and consumer brands advancing while large-cap technology companies declined.

Bank stocks contributed meaningfully to that Dow move as dividend increase announcements created buying interest from income funds, passive rebalancers, and directional investors waiting for the stress test catalyst.

Financial stocks are less sensitive to the discount rate pressure that compresses high-multiple technology valuations when rate-hike expectations rise. When the market is pricing in a potential Fed move before year-end, money moves toward sectors that benefit from elevated rates rather than away from them.

What to Watch in Bank Earnings Starting in July

Bank earnings season typically begins in mid-July with reports from JPMorgan Chase, Goldman Sachs, Bank of America, and Wells Fargo. Those reports will provide the first detailed look at how higher rates and the current credit environment are flowing through to actual reported earnings rather than analyst model projections.

Key metrics to track include net interest margin trends, loan growth rates, and credit loss provisioning levels across both consumer and commercial loan segments. Stable credit quality at elevated rates would confirm that consumer and business loan portfolios are holding up despite the significant borrowing cost burden visible in sectors like housing, automotive lending, and small business credit. Any signs of deteriorating credit quality would complicate the constructive bank stock thesis that stress test clearance and dividend increases have built.