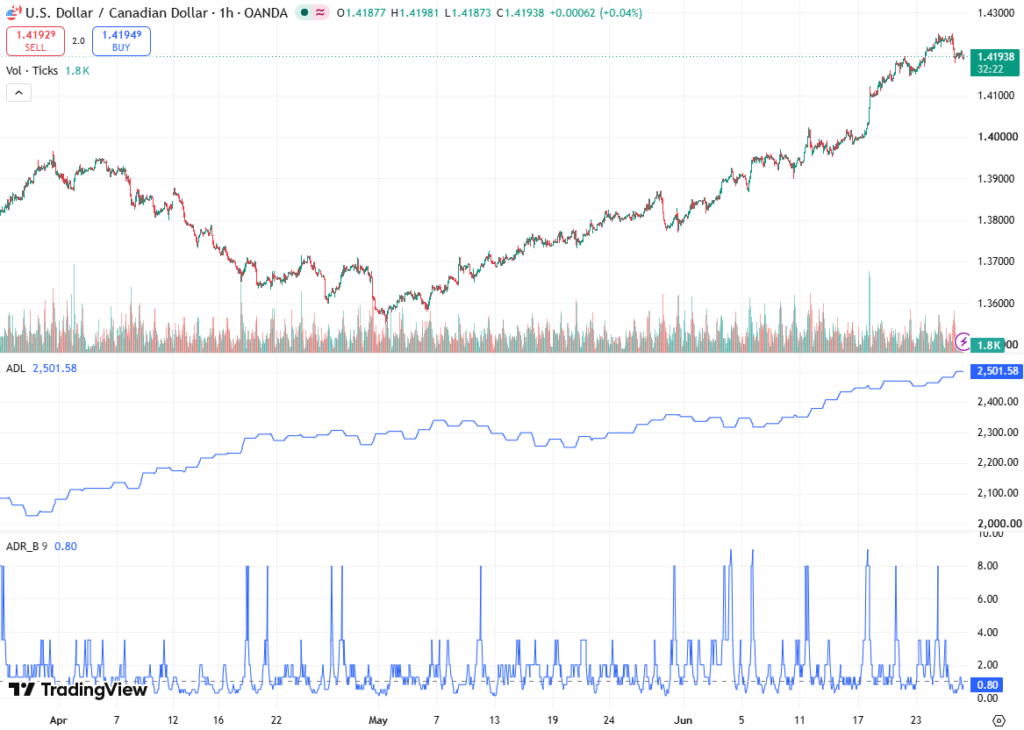

The USD/CAD exchange rate declined toward 1.4190 during Friday’s early European session, reflecting a shift in short-term rate differentials and positioning adjustments across USD macro portfolios. In this article, the brokers at Fonndure provide a comprehensive analysis of this topic.

The move extends a near-term corrective phase in the pair following rejection from the 1.4260–1.4280 resistance zone, with intraday momentum favoring USD downside pressure. Price action remains structurally contained within a broader consolidation range of approximately 1.4100–1.4300, with realized volatility contracting to multi-session lows.

The latest move is primarily driven by a recalibration of US terminal rate expectations following inflation data, rather than by any material change in Canadian macro fundamentals.

PCE Inflation Prints at 4.1% YoY, Signals Disinflation Deceleration

The latest data from the Bureau of Economic Analysis showed headline PCE inflation at 4.1% year-over-year in May, unchanged versus consensus projections but representing a marginal acceleration relative to prior disinflation trends observed in Q1. This marks the first print above 4.0% since April 2023, reinforcing sticky inflation dynamics at elevated levels.

Every month, PCE increased 0.4%, undershooting the 0.5% expected print, indicating a mild downside surprise in sequential price momentum. Core components continued to reflect uneven disinflation, with services inflation maintaining higher persistence than goods inflation.

From a policy transmission perspective, the Federal Reserve continues to monitor PCE as its primary inflation benchmark, with the latest readings implying that disinflation remains intact but non-linear, reducing urgency for additional near-term tightening.

Fed Rate Probability Curve Reprices Lower

Interest rate futures tied to the CME FedWatch Tool show a notable repricing in policy expectations. The probability of a 25 basis point rate hike in the July meeting declined from 34.2% to 28.9%, a 5.3 percentage point contraction in a single session.

This repricing reflects reduced tail risk for an immediate policy escalation, with the implied distribution of outcomes shifting toward a higher probability of a policy hold scenario. In rate markets, this adjustment has compressed short-end US yields by several basis points, contributing directly to USD depreciation pressure across G10 pairs, including CAD.

The front-end curve now embeds a flatter tightening trajectory, with implied terminal rate expectations adjusting lower by approximately 5–10 bps across the July–September horizon.

Bank of Canada Maintains Neutral-to-Flexible Policy Stance

The Bank of Canada continues to maintain a restrictive but adaptive policy framework. Recent minutes indicate consensus among policymakers to preserve policy optionality, particularly in response to asymmetric risks stemming from external trade policy shocks and energy-driven inflation volatility.

Market-implied expectations for additional tightening have compressed significantly. Current pricing reflects approximately 17 basis points of cumulative tightening by year-end, down sharply from roughly 60 basis points priced one month prior, representing a 70% reduction in tightening expectations.

This repricing aligns BoC expectations more closely with a prolonged policy hold regime, limiting CAD upside derived from domestic yield expansion.

Interest Rate Differential Compression and FX Implications

The USD/CAD trajectory remains highly sensitive to changes in the US–Canada yield spread, particularly at the 2-year tenor, which is a key driver of spot valuation models.

Recent moves show US short-end yields falling after inflation data, while Canadian rate expectations are dropping more sharply. This leads to only a partial offset in the narrowing of yield differentials.

Despite USD weakness, the absence of aggressive BoC tightening prevents a structural breakout in CAD strength. As a result, the pair continues to exhibit mean-reverting behavior within a defined liquidity band.

From a positioning standpoint, leveraged accounts have reduced net USD long exposure, but CAD speculative accumulation remains limited due to subdued domestic rate catalysts.

Technical Structure and Momentum Indicators

From a technical perspective, USD/CAD remains below its short-term 21-period moving average, signaling persistent bearish momentum on intraday frameworks. The RSI (14-day) has retreated toward neutral territory near 48–50, indicating loss of upside momentum without entering oversold conditions.

Immediate support is observed near 1.4160, corresponding to prior breakout consolidation levels, while secondary support is positioned near 1.4100, a key structural pivot zone. Resistance remains concentrated at 1.4260, with stronger supply density near 1.4300, where previous distribution phases occurred.

Volatility compression suggests a potential range expansion event in response to upcoming macro catalysts, particularly US consumer sentiment data.

Conclusion: Macro Repricing Dominates FX Direction

The decline in USD/CAD toward 1.4190 is primarily a function of front-end US rate repricing following softer-than-expected PCE momentum, rather than a CAD-specific strength cycle.

With Fed hike probability reduced to 28.9%, combined with BoC tightening expectations falling to 17 bps, the pair remains locked in a compressed interest rate differential environment. This creates a structurally neutral but tactically USD-weak bias, with price action likely to remain highly sensitive to incoming data releases.