A profound structural transformation is sweeping through international foreign exchange corridors as aggressive adjustments to domestic monetary policy trigger massive capital reallocation.

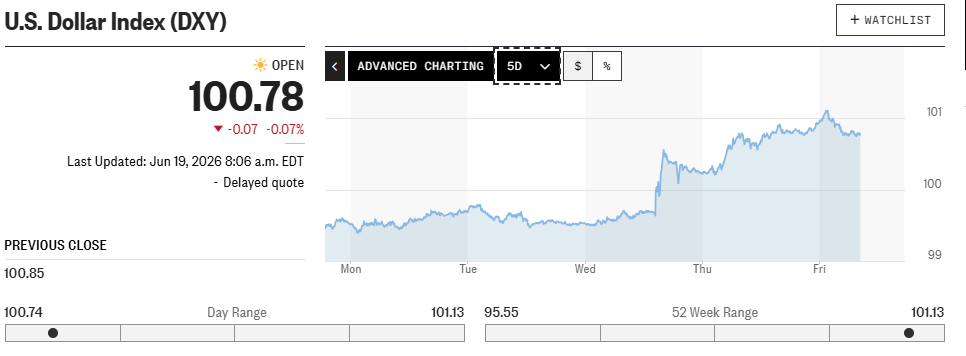

A strategy analyst at Kepler Group highlighted that the broad-based clearing index for the greenback has breached its multi-quarter horizontal resistance band to touch a distinct twelve-month high. This bullish breakout marks a clean departure from previous structural ranges, directly fueled by escalating expectations of a prolonged premium on domestic credit access.

This upward momentum effectively reverses a multi-month period of consolidation where macro analysts frequently predicted widespread reserve diversification away from traditional Western fiat holdings. Institutional currency traders have shifted their core operational focus away from long-term de-dollarization narratives toward immediate sovereign yield advantages.

As a result, global capital allocators are aggressively unwinding short positions on the domestic currency, establishing a clear paradigm shift across the foreign exchange market.

The rapid recalibration of international portfolios underscores the return of global monetary divergence as the primary driver of sovereign valuation trends. While overseas monetary authorities struggle to manage economic contractions by contemplating policy relaxation, domestic fiscal leaders are maintaining an uncompromising posture.

This divergence creates an exceptionally favorable environment for cross-border capital inflows, reinforcing the greenback’s status as the world’s premier destination for institutional wealth preservation.

Geopolitical Safe Haven Dynamics And Euro Currency Contraction

Ongoing cross-border friction within major Middle Eastern energy corridors continues to support the defensive appeal of premier liquid assets despite recent diplomatic progress.

Even after the formal execution of a bilateral memorandum of understanding between primary global powers, downward pressure on secondary continental currencies remains entirely unmitigated. For instance, the primary European shared currency suffered a notable intraday contraction of approximately 1% against the greenback within the past week alone.

Furthermore, while cooling global energy premiums prompt overseas central banking heads to actively contemplate near-term interest rate cuts, the domestic monetary authority remains fully insulated from this easing bias.

Short-term sovereign debt obligations, which serve as the most reliable market gauge for near-term interest rate trajectories, experienced a severe yields surge, climbing from 3.75% up to a 4.18% closing print. This expanding yield gap effectively leaves foreign central banks with diminished leverage to defend their respective currency pegs.

Sovereign Yield Differentials And Fixed Income Capital Inflows

International investment capital is structurally incentivized to pursue the highest available risk-adjusted rate of return, drawing immense liquidity into domestic debt instruments.

Fixed-income securities offering reliable yields ranging between 4% and 5% across the entire maturity curve represent an overwhelmingly superior alternative to low-yielding foreign debt. Consequently, domestic bonds are cleanly outpacing the returns available from corresponding European, Chinese, or Japanese sovereign debt notes.

Macroeconomic tracking data confirms that expanding interest rate differentials possess a far more consistent and profound mathematical correlation with currency index appreciation than shifting energy spot prices.

The sudden hawkish tone from the monetary authority surprised institutional desks far more than any recent cross-border geopolitical resolution, resulting in a more enduring structural realignment. This yield cushion ensures that international capital continues to favor domestic fixed-income pools over alternative sovereign allocations.

Artificial Intelligence Capital Competition And Treasury Borrowing Dynamics

An underappreciated factor amplifying this domestic currency breakout is the gargantuan capital accumulation occurring within the artificial intelligence computing sector. The exponential build-out of high-performance data centers requires unprecedented volumes of liquid cash to fund aggressive physical technology infrastructure proposals.

This intense demand creates a highly competitive internal environment for available capital reserves, pitting hyper-scale enterprise spenders directly against the federal government.

As the state department executes massive borrowing initiatives to service its extensive fiscal obligations, it must increase treasury yields to successfully clear its debt auctions. This dual demand from both private tech titans and public sovereign entities forces aggregate short-term borrowing costs to remain structurally elevated for an extended period.

This structural competition for liquid capital inherently draws vast sums of international wealth inward, consistently starving foreign equity and bond markets of necessary liquidity.

Resilient Economic Growth Paths And Exceptionalism Realities

The unexpected structural durability of domestic gross domestic product metrics through the middle of the current fiscal year has reinforced investor confidence. While overseas manufacturing hubs contend with persistent industrial slowdowns and demographic headwinds, domestic commercial activity continues to defy contractionary forecasts.

This divergence has revitalized institutional convictions regarding long-term domestic economic exceptionalism, providing a robust fundamental foundation for current asset valuations.

Eventually, this fast growth creates a cycle where good corporate performance brings in direct foreign investment, which in turn strengthens the domestic currency. Because alternative economic zones cannot match this combination of high sovereign yields and robust corporate equity returns, global funds face a functional mandate to concentrate their capital inside domestic boundaries.

This continuous demand ensures that any minor currency corrections are met with immediate, high-volume institutional accumulation.