Q1 earnings season is in the books for the hospital chains industry, and the results tell two very different stories depending on whether you’re looking at the income statement or the stock chart. Brokers from Byronixel dug into the numbers behind HCA Healthcare (NYSE: HCA) and its peers to make sense of the disconnect.

A Sector Built on Steady Demand, Squeezed From Every Angle

Hospital operators benefit from highly predictable demand, supported by an aging population and increasing rates of chronic illness, which help sustain patient volumes over time. However, profitability remains challenged by rising labor costs, regulatory compliance requirements, and dependence on government and private insurance reimbursement rates, limiting pricing flexibility.

Looking ahead, several tailwinds could support growth, including higher healthcare utilization and the adoption of AI-driven predictive analytics for treatment planning, staffing, and resource allocation.

At the same time, the industry faces meaningful risks from labor shortages, rising wage pressures, significant technology investment needs, and the possibility of regulatory changes or reimbursement cuts that could further pressure margins.

The Numbers Beat, the Stocks Didn’t Care

Across the four hospital chain stocks tracked this quarter, the group delivered a 0.7% revenue beat versus consensus estimates, a modest but still meaningful upside on the reported period.

However, the tone shifted quickly with forward expectations. Next-quarter guidance came in 2.7% below analyst expectations, creating a clear disconnect between near-term performance and the outlook embedded in valuations.

That combination of a backward-looking beat paired with a forward-looking miss is typically what drives sharp repricing in sectors where investors prioritize visibility over historical results. In this case, the market response has been notably negative. The group’s stocks are down an average of 14.8% since reporting earnings, reflecting elevated sensitivity to guidance rather than headline earnings strength.

What stands out is not weak execution, but the way expectations have reset. Even companies that posted solid operational results were caught in the same downward move, suggesting the sell-off is being driven more by macro-level caution around margins, labor pressures, and reimbursement trends than by isolated company issues.

As a result, short-term sentiment has decoupled from quarterly performance, placing greater emphasis on whether guidance stabilizes in the next reporting cycle.

HCA Healthcare: Solid Quarter, Harsh Reaction

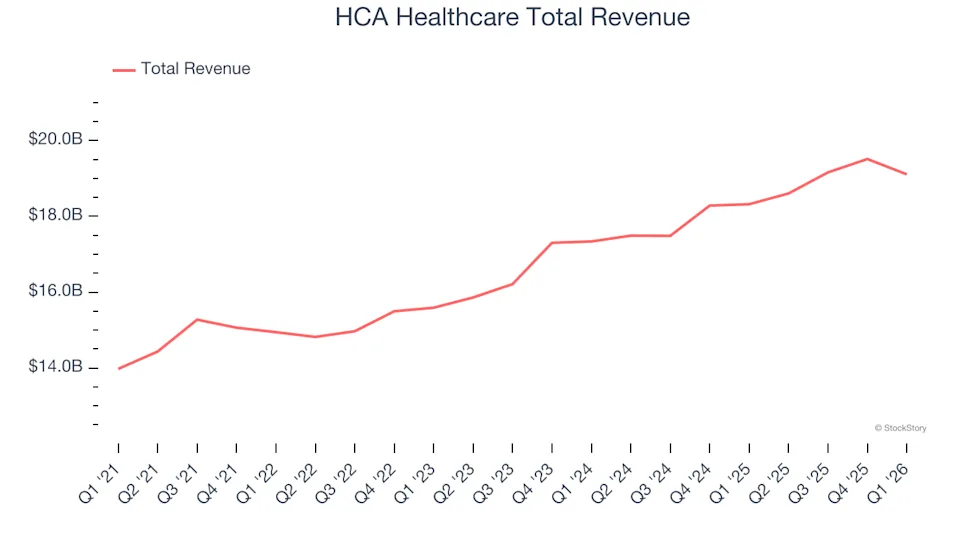

HCA Healthcare, which traces its roots back to 1968 and now operates 190 hospitals and more than 150 outpatient facilities across 20 U.S. states and England, reported revenue of $19.11 billion, up 4.3% year over year.

The figure came in in line with analyst expectations, with earnings per share also roughly matching forecasts, marking a quarter best described as steady rather than spectacular.

CEO Sam Hazen struck an upbeat tone, crediting the company’s workforce for navigating a shifting operating environment while continuing to deliver for patients and communities.

Despite the solid results, the market reacted negatively: HCA shares are down 20.6% since the report, with the stock trading around $376.26. The disconnect suggests investors are responding less to company-specific performance and more to broader sector-wide guidance concerns than to anything directly wrong in HCA’s underlying results.

Universal Health Services: The Quarter’s Standout Sort Of

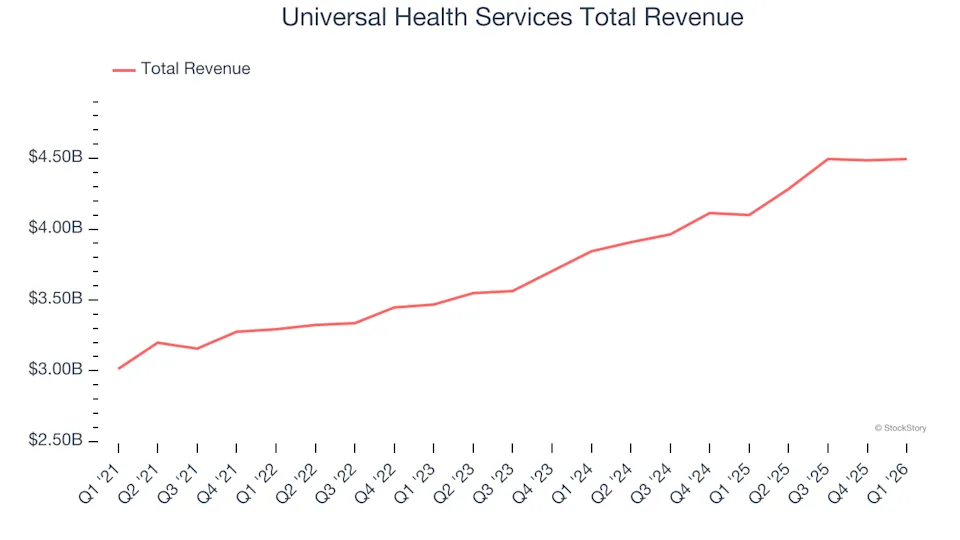

If any hospital chain had a genuinely strong quarter, it was Universal Health Services (NYSE: UHS), which operates acute care and behavioral health facilities across 39 states and three countries. UHS reported revenue of $4.50 billion, up 9.6% year over year and beating analyst estimates by 2.4%, the largest revenue beat and fastest growth rate among its peers, paired with an EPS beat as well.

Even that wasn’t enough to satisfy the market. UHS shares are down 21.5% since reporting, currently trading at $140.99, a steeper decline than HCA’s, despite delivering the stronger quarter on paper.

That widening gap between fundamental performance and stock reaction is the clearest signal yet that the sell-off is being driven more by sector-wide guidance concerns than by company-specific execution issues.

Outlook: A Sector Sell-Off Driven by Guidance, Not Fundamentals

The pattern across both names points to the same conclusion: investors are pricing in the 2.7% guidance miss far more heavily than the 0.7% revenue beat that preceded it.

That reaction reflects a reasonable instinct in a sector facing real headwinds labor costs, reimbursement pressure, and infrastructure spending all steadily erode margins over time but it also means the strongest performer in the group, Universal Health Services, was still punished nearly as severely as the in-line performer, HCA Healthcare.

For investors, that disconnect is worth watching closely heading into next quarter’s results. A sector-wide re-rating driven by macro guidance concerns can easily create mispricing at the individual stock level, especially for operators that are still executing effectively beneath the surface.