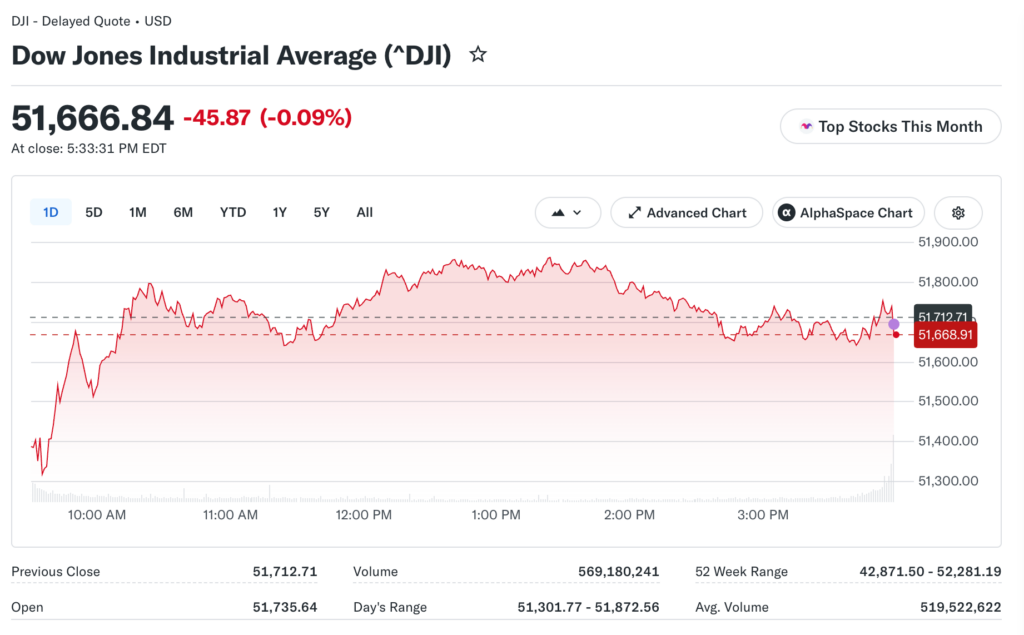

Four major market benchmarks moved in four different directions on June 23, 2026, and the spread between them was far wider than a single bad session for technology stocks would normally produce. The Nasdaq shed 2.21% and the S&P 500 fell 1.44%, while the Dow Jones Industrial Average lost just 0.09% and the Russell 2000 declined a relatively contained 0.96%.

The brand’s senior financial advisor mentions that Nummvix has been tracking this kind of internal market divergence as a structural read rather than daily noise, and June 23 delivered one of the cleaner examples of it in months.

Why the Dow Barely Moved When the Nasdaq Lost More Than Two Percent

The answer sits in index construction. The Dow’s thirty components skew heavily toward industrials, financials, and consumer businesses. Those categories carry lower valuation multiples and generate a larger share of their earnings from near-term operations rather than from long-range projections that discount rate changes can rapidly deflate.

The Nasdaq, by contrast, is dominated by technology companies whose valuations embed years of future cash flows at growth rates that assume a benign rate environment.

When a Bank of America research note warned of up to three rate hikes before year-end, selling pressure fell disproportionately on stocks whose valuations depend most on contained borrowing costs.

On June 23, fourteen of the Dow’s thirty components closed in positive territory while the technology sector dropped more than four percent, a contrast that headline index watchers missed entirely.

Sectors That Made Money While Tech Lost It

Real estate investment trusts moved higher on June 23, which runs counter to the instinct that a day driven by rate-hike fears should punish rate-sensitive assets first.

The more accurate read is that REITs rising signals the market is pricing the three-hike scenario as a tail risk rather than a central case. If institutions genuinely believed three hikes were coming, REITs would have been among the hardest-hit names rather than among the session’s quiet winners.

Healthcare also advanced, and the explanation here is more straightforward. When high-multiple technology stocks reprice on macro uncertainty, capital that needs to stay in equities migrates toward businesses generating predictable near-term earnings from established product lines. Healthcare fits that description precisely.

Its valuation does not stretch far into the future the way AI infrastructure stocks do, which makes it a natural destination for portfolio managers reducing duration within an equity-only mandate. That behavioral pattern has now appeared consistently across three separate sessions since the June 17 Fed decision introduced rate-hike expectations back into the market.

What Energy Stocks Did While Oil Fell Three Percent

The energy sector closing higher while crude oil prices dropped roughly three percent on Iran ceasefire progress is the most instructive divergence within a session already full of them. Upstream producers, companies that pull oil from the ground and sell it at commodity prices, faced direct pressure from the crude decline. But the refining subsector operates on a different economic equation.

Refiners profit from the spread between crude input costs and the refined product prices they charge customers. When oil falls faster than gasoline prices, that spread widens and refining margins expand. Investors holding broad energy exposure should check whether their positions tilt toward production names like Diamondback Energy, which face direct commodity price headwinds, or toward refinery-weighted companies that benefit when crude retreats.

The Memory Sector Showed Its Own Internal Split

Even within technology, June 23 demonstrated that sector-level and stock-level signals can point in opposite directions and both be analytically valid.

The DRAM ETF reached a fresh record high on the same day Micron Technology’s individual shares fell more than eleven percent. These two facts coexisted because they reflect different investor calculations operating simultaneously.

The ETF move reflects a collective view that AI memory demand remains structurally intact regardless of what any single company reports. Micron’s decline reflects specific uncertainty about one earnings report landing after the close on June 24. When those two signals diverge so sharply, the resolution comes quickly from whichever catalyst arrives first.

Building a Portfolio That Could Handle June 23

The session functioned as a live stress test for different portfolio construction approaches. A portfolio built around Nasdaq-weighted technology concentration absorbed the full force of the AI cost selloff and finished the day meaningfully lower.

A portfolio distributed across industrials, healthcare, financials, consumer names, and select energy positions saw those non-technology holdings provide genuine offset rather than simply theoretical diversification on paper. That difference between theoretical balance and actual buffer performance is exactly what June 23 made visible in real time.

The Morningstar barbell framework, which pairs meaningful technology exposure with an equivalent allocation to value and quality names in lower-duration sectors, held up more effectively than either a concentrated growth bet or a fully defensive posture. For investors reviewing their positioning heading into Micron’s June 24 earnings and the May PCE print on June 26, June 23 provided a useful blueprint for what allocation decisions look like under real pressure rather than in theory.