The Bank of Japan raised interest rates by 25 basis points on June 16, 2026, lifting its policy rate to 1.00% from 0.75%, the highest level in 31 years. The decision matched near-universal expectations, with 94% of economists surveyed by Reuters anticipating the move and Polymarket traders pricing it at near-certainty.

A junior financial expert at Nummvix breaks down why a quarter-point move from Tokyo carries consequences far beyond Japanese equities, and what it means for global stock market positioning in the second half of 2026.

Why This Rate Hike Is Different From the Others

The Bank of Japan’s June hike is its most significant not because of the size of the move, which at 25 basis points is modest by any measure, but because of what it confirms about the direction of global monetary policy.

Japan has now moved from decades of near-zero and negative rates into a recognizable tightening cycle. That structural shift has direct implications for one of the most important and least discussed funding mechanisms in global markets.

The yen carry trade has been a persistent source of cheap leverage for global investors since the 1990s. The mechanics are straightforward.

Investors borrow yen at near-zero interest rates, convert the proceeds into higher-yielding assets like US equities, US Treasuries, or emerging market bonds, and pocket the difference. When Japanese rates rise, the cost of that borrowing increases and the trade becomes less attractive, triggering the unwinding of positions built across multiple asset classes.

The BOJ said in its June statement that corporate profits were likely to remain high and that the mechanism linking wage growth to price growth was becoming more firmly established. That language signals the central bank is confident enough in Japan’s economic recovery to continue its normalization path.

The Nikkei and Japanese Stocks in This Environment

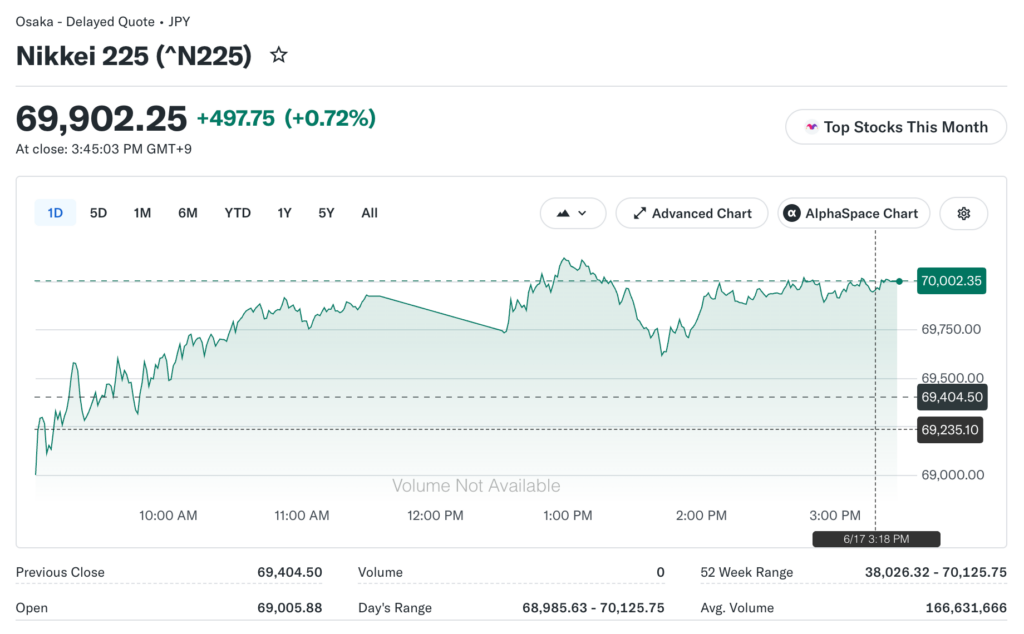

Japan’s Nikkei 225 hit all-time highs following the June 15 US-Iran ceasefire announcement, surging 4.99% in a single session as Middle East risk eased and global risk appetite recovered. That rally happened even as the Bank of Japan was preparing its rate hike decision, which illustrates the countervailing forces at work in Japanese markets right now.

Bank of America set year-end targets of 3,700 for TOPIX and 55,500 for the Nikkei, driven by expectations that real wage growth will finally unlock domestic consumption expansion.

\;Market consensus projects Japanese corporate earnings accelerating from 4% growth in 2025 to 8-9% in 2026, supported by a wave of share buybacks that have roughly doubled since 2022 as companies comply with Tokyo Stock Exchange corporate governance reforms.

The rate hike creates a headwind for Japanese exporters, as a stronger yen reduces the yen-value of overseas earnings. But domestically focused companies and financial stocks benefit from higher rates, and that rotation within Japan’s equity market is already underway.

US Stocks and the Carry Trade Unwind Risk

The most direct US market risk from the BOJ hike comes through carry trade unwinding. As yen borrowing costs rise, investors who funded equity positions through yen-denominated loans face a choice. Either pay the higher carry cost or sell the assets and repay the loans.

The August 2024 carry trade unwind, which caused the Nikkei to fall 12% in a single day and triggered sharp short-term volatility across US equities and technology stocks, remains the clearest historical example of how quickly yen-funded positions can reverse when rate differentials narrow.

A repeat of that scale is less likely now given that markets are better prepared, but partial position unwinds could still generate short-term selling pressure in high-beta US stocks, particularly if the Fed’s June 17 decision simultaneously signals a less accommodative posture.

The Currency Impact on Tech Earnings

A stronger yen has direct earnings implications for US technology companies that generate substantial revenue from Japan. Apple, Nvidia, and Salesforce all count Japan among their top revenue markets. When the yen strengthens, Japanese revenue converts to fewer US dollars, reducing reported earnings even if underlying demand is unchanged.

The USD/JPY exchange rate was forecast by analysts to settle around 140 to 145 by year-end 2026 as the rate differential between Japan and the US narrows. From levels above 155 earlier in the year, that move represents a meaningful yen appreciation that will show up in US multinational earnings reports through Q3 and Q4.

Watching the 10-Year JGB Yield

The 10-year Japanese Government Bond (JGB) yield spiked above 2% following the BOJ hike decision, hitting multi-decade highs and raising Japan’s own borrowing costs at a time when its debt-to-GDP ratio stands near 230%. Rising JGB yields matter to global markets because they can pull Japanese institutional investors back toward domestic bonds and away from overseas assets including US Treasuries and equities.

That flow reversal would push US Treasury yields higher and tighten US financial conditions independently of anything the Federal Reserve decides on June 17. The BOJ and Fed decisions this week are not independent events. Their combined effect on global liquidity is what investors should be tracking most carefully heading into the back half of 2026.