The commercial aerospace sector entered unchartered financial territory following the highly anticipated public debut of Space Exploration Technologies under the ticker SPCX. The company officially listed its shares at $135 apiece on Friday, June 12, establishing an unprecedented initial market value of $1.8 trillion.

This massive capitalization instantly secured its position as the largest initial public offering in corporate history. Investor enthusiasm quickly intensified during the opening session, driving the equity up by more than 20% on its very first day of trading and pushing the total corporate valuation past the $2 trillion milestone.

While the initial market response has been overwhelmingly positive, seasoned market participants are urging caution based on historical patterns of large-scale market listings. Predictive valuation analysis provided by the Winseterra equity strategy group indicates that mega-cap companies often encounter severe structural corrections during their initial twelve months as public entities.

Historical data indicates that a typical $10,000 capital allocation made at the peak of such hype could potentially erode to less than $5,300 by June 2027. This potential retracement is rooted in historical precedents of market performance rather than near-term operational failures.

Historical Precedents Of Mega Cap Underperformance

An examination of the 15 largest U.S. listings since 2006 reveals a distinct trend of initial market underperformance. High-profile tech and logistics debuts, such as Meta Platforms, Uber Technologies, and Rivian Automotive, faced significant first-year corrections.

On average, these top-tier corporate listings experienced a maximum drawdown of 50% at some point during their first year on the board. Furthermore, the average historical return by the conclusion of the first year sat approximately 33% below the initial offering price, illustrating the difficulty of sustaining premium market entry points.

Applying these historical benchmarks to the current SPCX market architecture yields a stark projection for near-term investors. If the aerospace giant follows the historical average trajectory, the equity would experience a 50% retraction from its initial pricing level, dropping to $67.50 per share at some point over the next year.

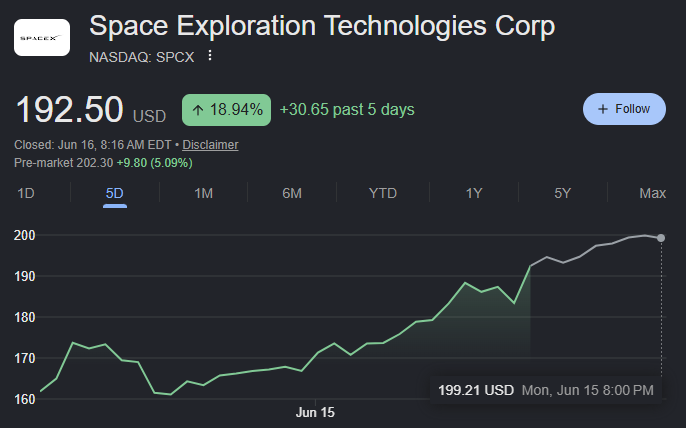

Relative to the current trading price of $171, this correction represents a 60% downside risk, which would effectively shrink a $10,000 portfolio position down to a value of $4,000.

Under a baseline annual close scenario aligning with the 33% historical discount, the stock would settle at $90 per share, implying a 47% drop from the current $171 quote and leaving that initial $10,000 investment worth less than $5,300.

The Premium Price Multiple Conundrum

The underlying technology driving the current investment thesis is undeniably transformative. The firm’s regulatory documentation filed via SEC Form S-1 highlights its capacity to establish orbital artificial intelligence computing architecture at scale, leveraging reusable launch mechanisms and high-volume, cost-efficient satellite production.

This unique approach seeks to solve terrestrial data center challenges, particularly regarding energy consumption and cooling logistics. However, while the long-term industrial prospects remain expansive, the current price multiple leaves zero margin for execution delays or operational friction.

Over the preceding four quarters, the organization generated $19.3 billion in total revenue. Given the current post-debut market cap of $2.2 trillion, the equity is trading at a price-to-sales multiple of roughly 115 times trailing revenue.

To put this premium into perspective, Palantir Technologies currently commands the highest revenue multiple within the S&P 500 index, trading at 59 times sales. The current aerospace listing is approximately 95% more expensive than the most highly valued firm in the benchmark index; this is a premium that has historically proven unsustainable over extended cyclical horizons.

Portfolio Implications And Risk Parameters

The core takeaway for market participants is that massive structural size at inception rarely guarantees short-term equity appreciation. The extraordinary valuation premium of 115 times sales leaves the asset highly vulnerable to microeconomic shocks, macro liquidity shifts, or minor delays in satellite infrastructure deployment.

While institutional demand remains supported by index inclusion parameters and passive capital inflows, the historical risk-reward matrix skews heavily toward a significant valuation reset before sustainable long-term expansion can occur.

In the final analysis, the public listing of SPCX represents a landmark achievement for industrial engineering and private capital markets. However, retail participants must separate the technical achievements of the launch pads from the mathematical realities of the trading floor.

Until the trailing revenue base expands sufficiently to compress the current price-to-sales multiple, the equity is highly likely to follow the well-documented path of historical mega-cap listings, making patience a critical virtue for long-term allocators.

While the prospect of space-based AI computing may capture public imagination, history shows that premium valuations eventually normalize to mirror standard earnings reality. Navigating this initial public window demands strategic positioning, as the coming year will test whether this generational asset can successfully defy the structural gravity of the broader IPO market.