The domestic semiconductor fabrication landscape is experiencing a profound structural reallocation of capital as sovereign economic directives merge directly with private enterprise manufacturing pipelines. Institutional tech investors aggressively repositioned their portfolio exposure during extended hours trading following executive confirmations of a landmark production accord.

Investment researchers at Risance indicate that federal intervention has successfully driven massive consumer electronics conglomerates to secure localized processing agreements. This sweeping macroeconomic development is widely interpreted as a definitive validation of long standing industry rumors regarding the repatriation of microchip production.

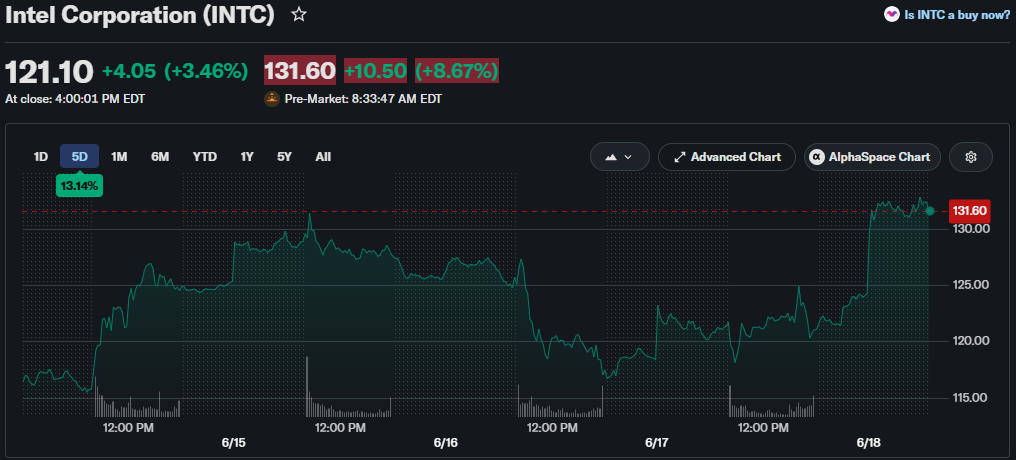

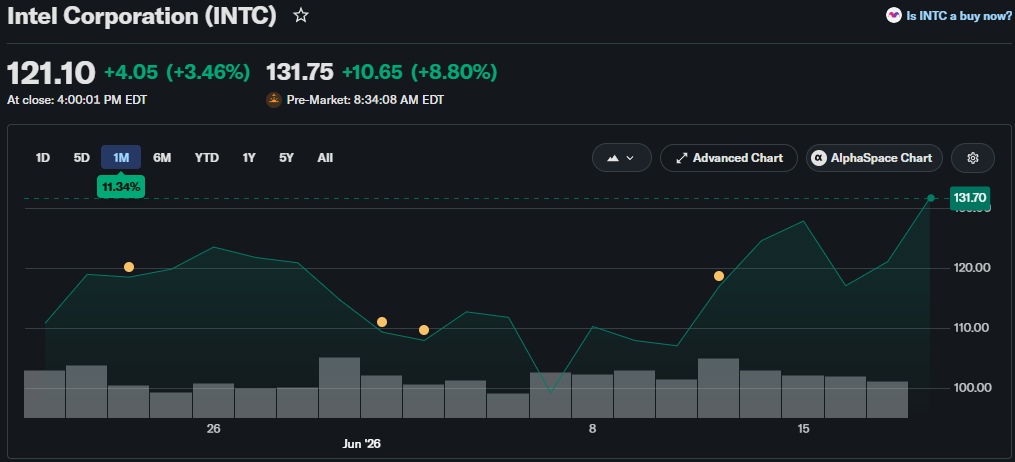

Following the formal announcement broadcast across state media channels in the early morning hours, equity contracts for the domestic chip pioneer surged by a substantial 5.7% during overnight market operations. Concurrently, public equity shares of the consumer hardware giant achieved a localized upward bump of 0.6% as index funds adjusted to the news.

Executive statements revealed that the federal government directly structured the agreement, highlighting a previous sovereign transaction that secured a strategic 10% equity stake in the manufacturing firm. Financial summaries indicate the chipmaker’s total market value has expanded from a baseline of $100 billion to over $600 billion.

The sovereign strategy focuses heavily on revitalizing domestic high tech manufacturing by aggressively funneling major technology firms toward independent regional foundries. Administrative disclosures indicate that federal dealmakers previously assisted in securing a tier one fabrication pact with a prominent artificial intelligence graphics leader.

Foundry Network Footprints And Regional Competitive Paradigms

The core infrastructure driving this massive domestic fabrication push is anchored by a flagship production hub situated on an expansive campus in Arizona. This highly advanced facility functions as the operational cornerstone for the organization’s external manufacturing services and deep tech lithography development.

Additional state side manufacturing assets are actively operating across established industrial sites in Oregon and New Mexico, alongside a massive new multi billion dollar development asset currently expanding in Ohio. Meanwhile, international competitors are rushing to finalize their own alternative silicon fabrication facilities in Taylor, Texas, which are projected to go operational later this calendar year.

The newly finalized manufacturing agreement marks a historic corporate reunion for the two technology giants, reviving an exclusive hardware supplier relationship that dissolved around the year 2020.

The consumer tech giant had previously relied on the domestic manufacturer to design and supply primary processors for its personal computing lines from the year 2006 onward before transitioning to in house architectures.

Advanced Process Milestones And Quantitative Performance Metrics

Crucial to the enterprise’s long term competitive positioning is the recent commercial unveiling of its highly advanced 18A-P manufacturing process architecture. Technical datasheets show that this newly updated iteration delivers up to a 9% increase in absolute processing performance alongside a noticeable 18% reduction in total power consumption.

Furthermore, the engineering updates yield a substantial 20% to 40% improvement in baseline thermal resistance compared to previous generations. The organization confirmed that this flagship process node has officially entered the critical phase of risk production, allowing engineers to gather extensive data on defect rates before launching full scale commercial manufacturing.

This rapid sequence of advanced technology announcements has pushed the enterprise’s equity performance to the very top of institutional market watchlists. Public trading data shows that the underlying stock has achieved an extraordinary 228% surge year to date, backed by highly explosive quarterly earnings data.

Recent corporate balance sheets highlight a 7% revenue increase to exactly $13.6 billion, outperforming consensus Wall Street expectations by a comfortable 9% margin. The specialized data center and artificial intelligence business unit drove the bulk of this growth, with total segment sales climbing a massive 22% to hit $5.05 billion.

Foundry Balance Sheet Adjustments And Retail Market Sentiment

Simultaneously, the financial overhead associated with running the independent foundry division has demonstrated highly encouraging signs of structural stabilization. The segment’s recorded quarterly operating loss narrowed significantly to exactly $2.4 billion, representing a clear $72 million improvement on a consecutive quarter over quarter basis.

Senior accounting desks attribute this fiscal progress to steadily improving wafer yields achieved across the brand’s core automated production lines. Despite these positive financial trends, general retail sentiment indicators remain firmly locked in neutral territory as market participants evaluate long term geopolitical execution risks.

Independent market analysts emphasize that securing the consumer hardware giant’s business could effectively double the manufacturer’s total annualized revenue run rate, which currently sits at approximately $53 billion. This massive influx of external corporate demand would completely transform the foundry from an internal cost center into a highly profitable global supplier.

Consequently, institutional portfolio managers view this specific development as the single largest operational victory within the modern semiconductor industry. As federal manufacturing directives continue to reshape international supply chains, the convergence of sovereign equity stakes and massive commercial foundry contracts will dictate global technology valuations.