The Federal Reserve held its benchmark rate steady at 3.50%–3.75% on June 17, 2026, but the decision itself was almost beside the point. All eyes were on the man delivering it. Nummixo‘s lead financial expert examines what Kevin Warsh’s debut as Fed Chair means for the S&P 500, Nasdaq, and Treasury markets heading into the second half of the year.

A New Chair, A Very Different Tone

Kevin Warsh was sworn in as the 17th Chair of the Federal Reserve on May 22, 2026, after a narrow 54–45 Senate confirmation vote. His first FOMC meeting on June 16–17 carried outsized significance from the moment it was scheduled on the calendar.

CME FedWatch data put the probability of no rate change at 97% as of June 13. That part was settled well before the meeting opened. What markets were actually watching was the updated dot plot, the Summary of Economic Projections, and every word from Warsh’s first post-meeting press conference.

Warsh has long been critical of the Fed’s reliance on backward-looking data like the Consumer Price Index and Personal Consumption Expenditures.

He has also signaled a preference for less prescriptive forward guidance, describing his ideal policy environment as one with “messier meetings” where real debate happens before decisions get locked in. That philosophical shift alone changes how investors should interpret any future statement from the central bank.

What the Dot Plot Revealed

The June dot plot carried more weight than usual this cycle. The previous version, released after the March meeting, projected just one rate cut in 2026. That baseline was already crumbling well before the June session opened.

May CPI came in at 4.2% year-over-year, driven by energy prices up 23.5% annually amid the ongoing Iran conflict. Food inflation added another 3.1% to the broader pressure. The labor market posted 172,000 jobs in May, well above consensus expectations and reducing any argument for near-term accommodation.

At least three FOMC voting members were projected by Bank of America economist Aditya Bhave to favor rate hikes before year-end. That marks a sharp shift from the cut-leaning stance markets assumed entering 2026. A committee that was debating the pace of cuts six months ago is now openly debating whether a hike becomes necessary before December.

The Communication Shift That Actually Moves Markets

Warsh has not committed to holding press conferences after every FOMC meeting, breaking from the practice Jerome Powell institutionalized over his tenure. That single procedural change adds meaningful uncertainty between policy meetings and forces markets to lean more heavily on incoming economic data.

Analysts flagged that Warsh may guide toward a “smaller role in day-to-day markets”, leaning into a more data-dependent and less communicative policy approach. If the Fed speaks less frequently, every statement carries more weight and bond markets will reprice faster on CPI and jobs data instead of waiting for Fed cues.

Schwab Center for Financial Research identified the removal of the “easing bias” from the policy statement as the most actionable signal for equity investors right now. Markets may have tolerated higher rates while believing cuts were eventually coming. If that expectation disappears entirely, valuations across growth-heavy portfolios face a meaningful reset in the months ahead.

Treasury Yields and What They Tell Stock Investors

The 2-year Treasury yield sat at 4.052% and the 10-year at 4.461% heading into the June 17 decision. That spread reflects a market pricing near-term restraint without yet betting on a sharp economic slowdown arriving soon.

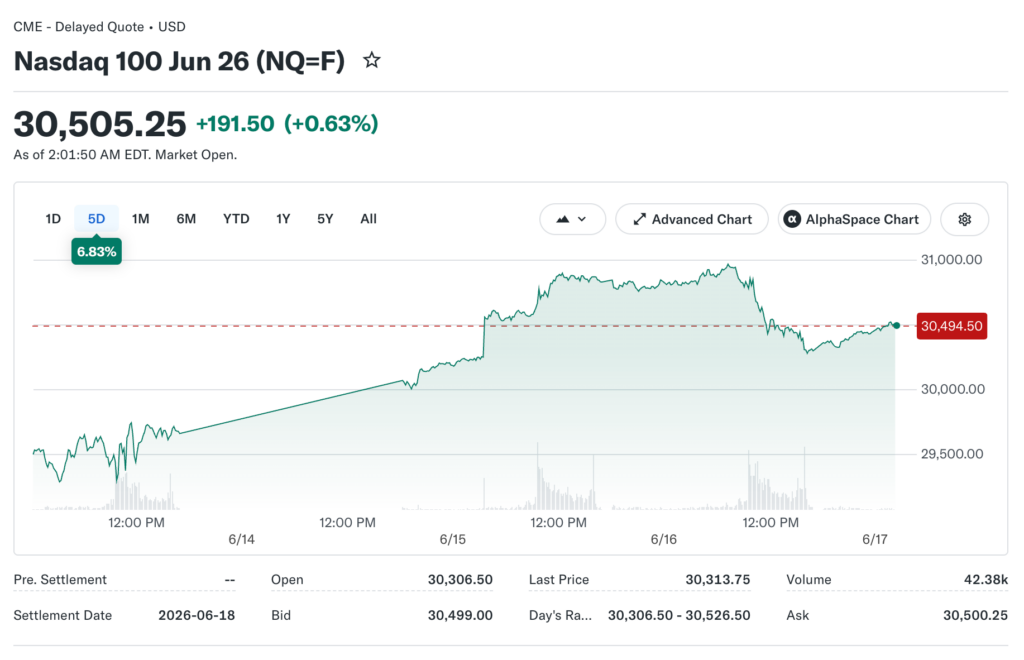

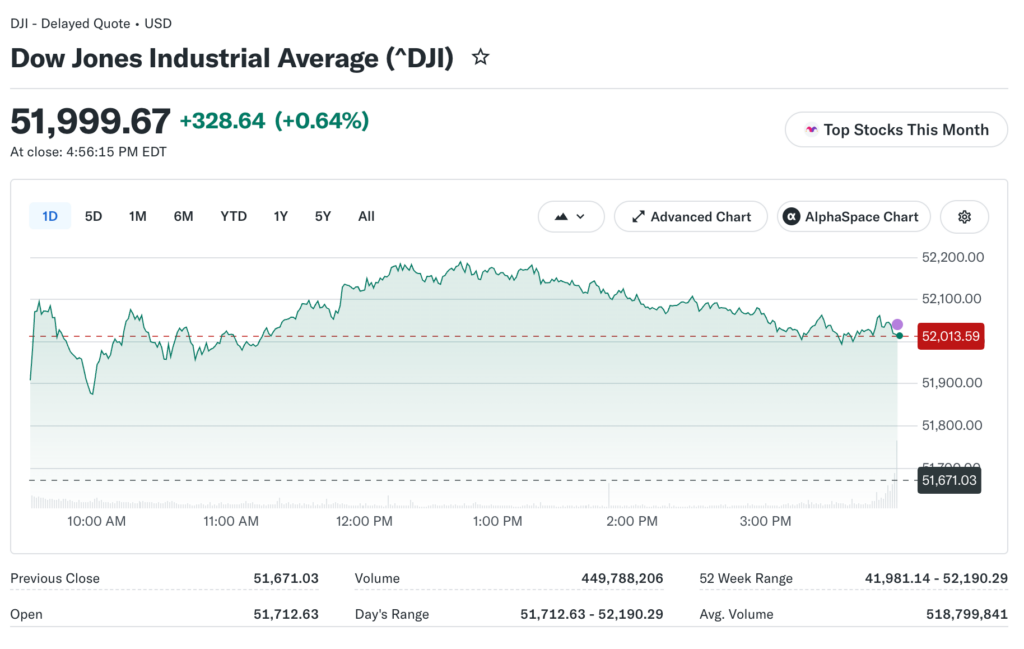

The Dow Jones Industrial Average closed above 52,000 for the first time on June 16, adding 329 points, even as the Nasdaq fell 1.15% and the S&P 500 slipped 0.08%. That divergence is meaningful and deliberate, pointing to rotation out of high-multiple tech into industrial and value names rather than any signal of broad economic confidence.

Reading the Room Before September Arrives

The Fed’s June meeting is less a pivot moment and more a recalibration of rate expectations across the investment community. With inflation at 4.2% and energy costs structurally elevated by the post-Iran conflict environment, the central bank needs hard evidence before it moves in either direction.

Investors should monitor the equal-weight S&P 500 relative to the standard cap-weighted version as a health check on the rally. A widening gap between the two signals increasing concentration risk, where a shrinking group of stocks does more of the market’s work. A narrowing gap signals broadening participation, which would be the healthier indicator for a sustainable move higher heading into Q3.

The next quarterly projection meeting arrives in September 2026, and between now and then every CPI print and jobs report becomes a de facto Fed policy signal. Positioning for uncertainty rather than conviction is the clearest takeaway from Warsh’s first month leading the central bank in genuinely difficult inflationary conditions.