Investors arriving at their screens on June 24, 2026 faced a market environment built from at least three separate stories running simultaneously, each with its own timeline and its own implications for rate expectations, equity valuations, and sector rotation.

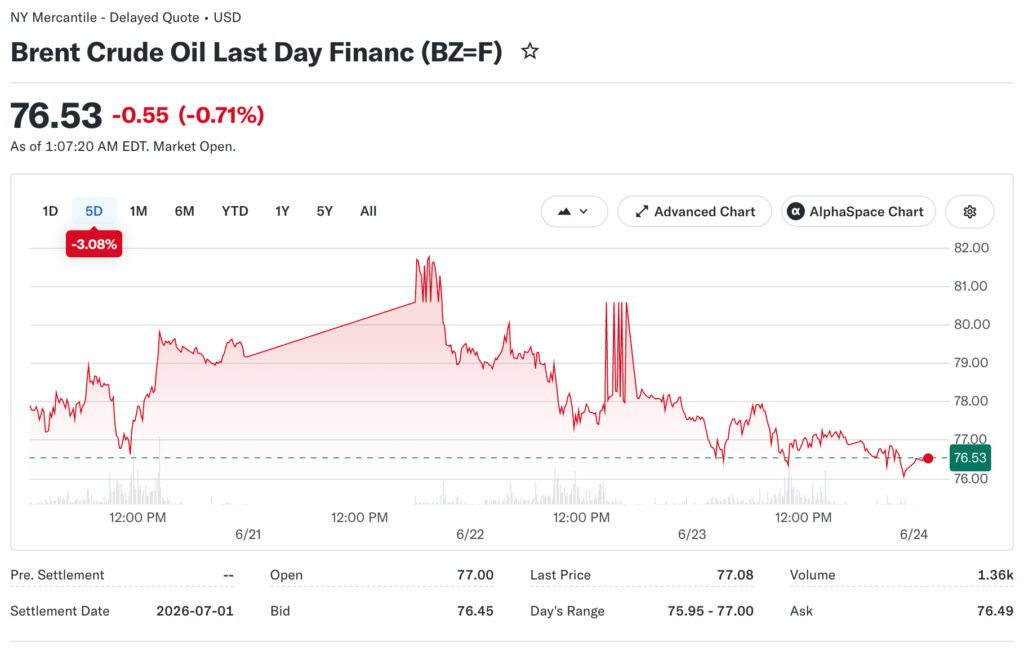

Brent crude had slipped to $75.13 on June 23, the Swiss peace negotiations between the US and Iran were producing the most encouraging language yet from the Iranian side, and a Bank of America research note warning of up to three rate hikes before year-end was still reverberating through technology stocks.

A lead broker at Nummvix discusses how these threads interact with each other and with the week’s remaining data releases, and why June 24 sits at an unusually consequential intersection for equity market positioning across virtually every sector and asset class.

The Oil Price Retreat and What It Does to the Inflation Math

Brent crude at $75.13 on June 23 represents a meaningful shift in the Federal Reserve’s inflation management environment.

Research from the Federal Reserve Bank of Dallas calculated that the Iran war’s energy disruption added roughly 1.7 annualized percentage points to headline PCE inflation during the first quarter of 2026, a push the Fed could not address with rate hikes without simultaneously tightening into a geopolitical supply shock.

With oil retreating from conflict highs above $100, the May PCE report due June 26 should begin to reflect that energy cost relief.

The distinction that matters for rate-hike probability is whether relief shows up as a deceleration in the year-over-year rate or an active month-over-month decline. The former gives the Fed reason to pause. The latter gives the Fed reason to delay hike consideration considerably further into 2026.

Why the Bank of America Note Hit Harder Than Its Base Case Justified

The Bank of America research note circulating on June 23 was a scenario analysis, not a forecast. It outlined conditions under which three hikes before December would become necessary rather than a single one, and markets responded to it as though it were a prediction.

Rate-hike probability for at least one move by year-end had already climbed to 50 percent, up from 24 percent in early April, before the note added anything new.

High-multiple technology names, which had not fully digested even the single-hike probability, bore the brunt of the selling. The three-hike tail risk introduced a worst-case ceiling the market felt compelled to partially price without treating it as the base case.

The PMI Reading That Should Have Moved Markets More

Flash PMI data for June landed on June 23 morning and came in above expectations on every measure tracked. The Composite Index reached 52.2, Services came in at 51.3, and the Manufacturing Index hit 55.7.

That Manufacturing reading is meaningfully above the 50-level threshold separating expansion from contraction, and historically a print in the mid-50s would anchor an entire day’s market narrative around industrial demand strength and its implications for forward corporate earnings estimates.

On June 23 it generated almost no discussion, as the Bank of America note and the semiconductor selloff consumed all available analytical attention. When constructive fundamental data gets repeatedly ignored in favor of macro fear, the resolution historically favors the fundamentals once the fear catalyst either confirms or fails to materialize. Micron on June 24 and PCE on June 26 gave the week two opportunities to test that thesis directly.

What Tehran’s Language Actually Signals for Markets

Iran’s foreign minister described major progress in the Swiss talks on June 23, and the specific phrasing carried more weight than a casual diplomatic update might suggest.

Iranian officials had been notably careful throughout the ceasefire process to preserve the option to withdraw. Language of major progress from that side of the table represents a different register than the qualified diplomatic hedging that had characterized earlier communications.

For markets, more confident Iranian language reduces the probability of a ceasefire collapse that would send oil back toward $100. It also increases the odds that May PCE captures genuine energy cost relief rather than a temporary dip that reverses before publication, and continues unwinding the geopolitical risk premium embedded in energy production stocks and defense sector names.

Reading the Setup Before the Catalysts Hit

Micron’s fiscal Q3 results arriving after the close on June 24 carry the most concentrated power to shift the week’s narrative. Consensus calls for revenue of $34.66 billion and EPS of $19.95. A result that clears those expectations and confirms AI memory supply remains fully allocated would directly contradict the AI spending concern Bank of America’s note amplified on June 23.

The confluence of oil below $80, constructive PMI data, and advancing Iran talks describes a macro backdrop that should logically support risk assets.

How much of that constructive context was absorbed by the June 23 selloff, and how much remains as a genuine tailwind for sessions ahead, is precisely the question that Micron’s numbers and Thursday’s PCE reading are positioned to answer with actual data rather than with another round of analyst scenario modeling.