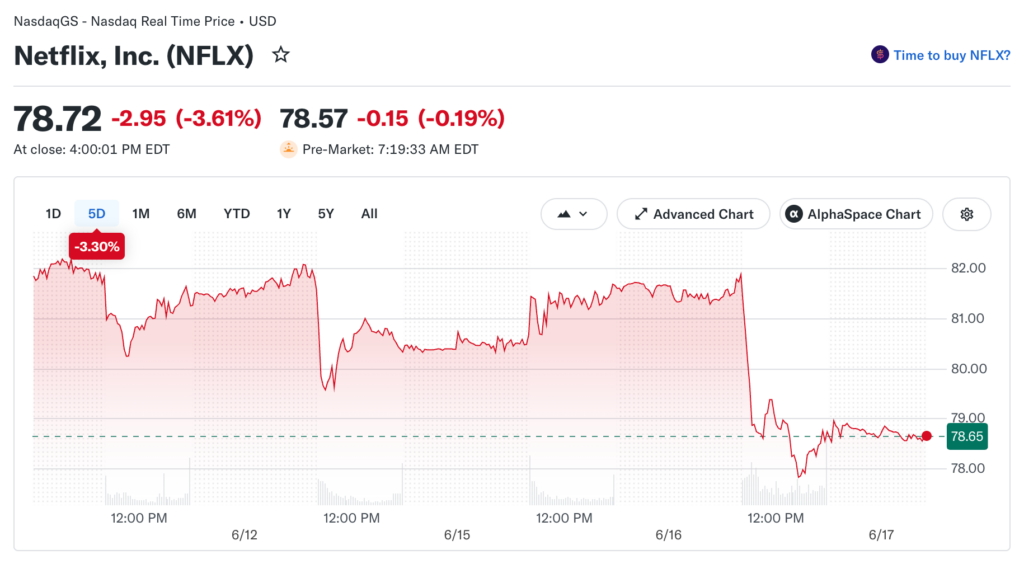

Netflix (NFLX) fell 3.68% on June 16, 2026, closing near $78.72 and sitting approximately 39% below its all-time high, even as the broader market posted mixed results around the US-Iran ceasefire news.

The stock’s disconnect from the relief rally that lifted technology names broadly on June 15 is not random noise, and the reasons behind it are worth understanding carefully before the next major catalyst arrives for the platform.

A lead financial expert at Byronixel emphasises that the selloff reflects a specific and layered set of valuation and macro pressures that are materially different from the challenges facing other large-cap technology names in the current environment.

What Is Actually Driving the Decline

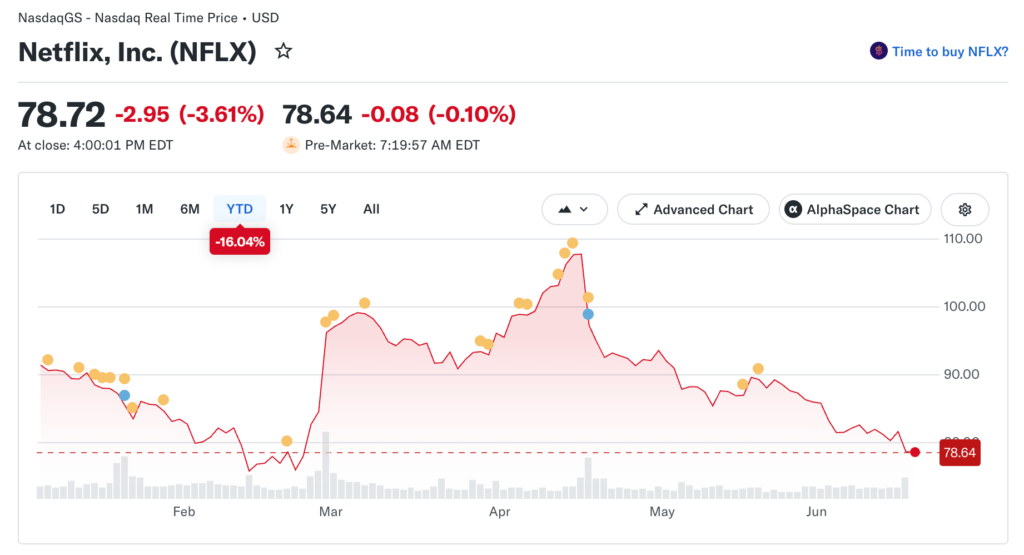

Netflix’s drop from its all-time high has accelerated meaningfully since the April 2026 earnings report. NFLX fell 25% since that report while the S&P 500 gained 4% over the identical period, a divergence that is not explained by subscriber loss or any visible weakness in the company’s core revenue metrics.

The company posted Q1 revenue of $12.25 billion, beating the $12.18 billion consensus estimate, with net income of $5.28 billion, more than double the $2.42 billion reported in the quarter before.

The problem is structural rather than operational: 10-year Treasury yields near 96th-percentile highs historically create a discount rate problem that strong quarterly results alone cannot overcome for a long-duration growth stock of Netflix’s profile.

When the rate used to discount future cash flows rises sharply, present value falls even if the underlying business is performing exactly as expected quarter after quarter. Netflix generates most of its investment value from earnings projected years into the future, making it more sensitive to this dynamic than shorter-duration businesses trading on near-term earnings multiples.

The Advertising Tier and What It Actually Means

Netflix no longer provides quarterly subscriber addition metrics, removing a key data point investors relied on to gauge platform momentum and health. What replaced it as the primary forward-looking growth indicator is advertising revenue, which analysts project will reach $3 billion in 2026 as the ad-supported tier continues to scale across major markets globally.

The June 16 expansion of Netflix’s exclusive partnership with iHeartMedia to roll out celebrity-focused video podcasts and live broadcasts adds a new content category but introduces genuine execution risk alongside the opportunity. Live and creator-led unscripted programming carries higher production and talent costs than traditional scripted content, and if the new formats fail to drive proportional engagement increases, they could pressure Netflix’s current 28.5% net income margin without delivering the advertising revenue lift intended.

Operating margins are projected to hit 31.5% in full-year 2026, and Q1 delivered in line with that trajectory. The core concern is whether the live content pivot can sustain that margin level as the cost structure shifts toward higher-variable-cost programming at meaningful scale.

Insider Activity and Prediction Market Signals

Institutional analysts have raised persistent concerns about Netflix’s growing reliance on aggressive price hikes rather than organic subscriber acquisition for recent revenue growth. Insiders have net-sold across 107 recent transactions, signaling limited conviction at current prices relative to the stock’s implied fair value as management sees it internally.

Prediction markets assign just 12% odds of NFLX reaching $90 by the end of June, which at current prices near $78 implies the market sees no near-term recovery catalyst of sufficient magnitude. The next scheduled earnings date is July 16, 2026, and both analyst consensus and prediction market probabilities will reset meaningfully around that single report.

What the Bull Case Actually Requires

Analyst price targets average $114 per share, representing substantial upside from the current $78 range. Mahaney at Seaport Research maintains a Buy rating citing ad-tier growth and international expansion as underappreciated revenue drivers, while Jefferies holds a similarly constructive view on the stock’s 12-month return potential.

The bull case requires two things happening simultaneously: 10-year yields retreating from near-record levels as the Federal Reserve signals an eventual easing path, and advertising revenue visibly accelerating in the Q2 report rather than remaining a forward projection disconnected from reported results. If yields stay elevated following the Fed’s June 17 decision, the discount rate problem does not resolve regardless of how well the business executes on a quarterly basis.

The Setup Heading Into July 16 Earnings

Netflix’s Q1 EPS beat of $1.23 versus the $0.76 consensus estimate was a 61.21% positive surprise, the kind of outperformance that normally generates a meaningful stock price rally in the session following the report. The fact that the stock continued declining after that beat reflects how completely the rate environment is overriding fundamental performance in determining NFLX’s near-term price.

Investors watching this setup should track the 10-year Treasury yield relative to 4.5% as carefully as they track Netflix’s own revenue and engagement metrics in the weeks before July 16. Both signals need to move in the right direction before the stock can mount a sustainable recovery from its current level.