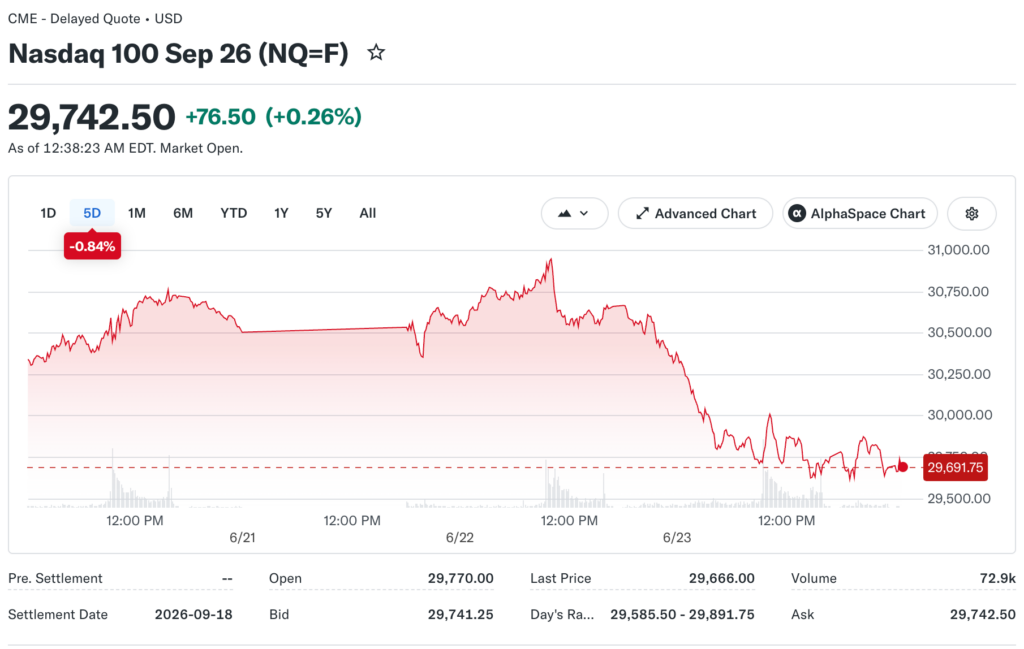

The Nasdaq Composite fell 2.21% on June 23, 2026, and the S&P 500 dropped 1.44%, marking the second consecutive session of broad technology declines heading into June 24. South Korean chip stocks triggered the selloff before US markets even opened, with the KOSPI falling nearly double digits and pulling semiconductor names lower across Asian, European, and US trading hours.

A senior financial analyst at Kepler-Group says what happened on June 23 is not simply a sector rotation but a stress test of the AI spending thesis that has driven markets all year.

What Started the Cascade Before the US Open

South Korea’s KOSPI index fell sharply overnight, dragged down by its heavy concentration in memory and chip stocks. That move bled directly into European markets and US futures before the New York session began, setting a defensive tone that the morning data did not fully reverse.

The PMI Composite Flash for June came in at 52.2, slightly above the prior reading of 51.7, suggesting the US economy remains in expansion. That constructive reading was entirely overshadowed by a Bank of America research note warning of up to three interest rate hikes before year-end and flagging narrowing market leadership as a growing vulnerability.

The Bank of America Note That Moved Markets

Bank of America’s research note on June 23 was the most discussed document in trading rooms across Wall Street for most of the session. The note argued that narrow leadership in AI and semiconductor stocks has left the broader index structurally fragile, and that elevated valuations combined with potential rate hikes create asymmetric downside risk on any guidance disappointment.

The Technology Sector within the S&P 500 fell 4.13% on June 23 alone, erasing gains from nearly 60% of the index’s other holdings in a single session. Alphabet and Oracle each slid 5%, dragging the Communication Services sector down 3.8%. NVIDIA tumbled 3.2% to $201.97.

Micron fell 11.4% to $1,074.60. Taiwan Semiconductor dropped 5.2% to $443.35. The VanEck Semiconductor ETF declined 6.5% to $625.62. Those moves together represent a coordinated repricing of AI infrastructure exposure rather than isolated company-specific reactions.

SpaceX’s Bond Deal Added Fuel to the Fire

SpaceX shares fell around 8% for a second consecutive session on June 23 after reports emerged of a proposed $20 billion bond sale. Investors who bought the IPO at $135 and watched shares peak at $225.64 were now looking at a stock that had entered bear market territory from its highs in less than a week.

The bond deal raised concerns about the company’s capital structure at a valuation many analysts had already flagged as aggressive.

SpaceX’s market cap remains above $2.3 trillion despite the declines, but the sequence of events, an IPO surge, an immediate bond offering at elevated prices, and a rapid correction, is a pattern that historically tests retail investor conviction and prompts institutional position trimming.

What the Divergence Between Sectors Is Saying

While technology led the decline on June 23, the session was more nuanced beneath the surface. Small and mid-cap indices posted modest gains. REITs, healthcare, and financial stocks all advanced. Energy names closed higher despite oil falling roughly 3% on continued Iran ceasefire progress.

That pattern mirrors what happened after the June 17 Fed decision, with investors moving away from high-multiple growth names and toward sectors with more near-term earnings visibility.

The DRAM ETF climbed to new highs on June 23 even as Micron’s individual stock fell more than 11%. That divergence reflects the market pricing in strong fundamental demand while repricing company-specific risk ahead of Micron’s June 24 earnings report.

Heading Into June 24 With Two Critical Reports Pending

Wednesday June 24 brings Micron’s fiscal Q3 earnings after the close, with consensus estimates projecting $34.66 billion in revenue and EPS of $19.95. That report follows the June 23 selloff that took Micron down more than 11%, which paradoxically means the stock enters its earnings release with a lower bar to clear than it held at the start of the week.

FedEx reported strong fourth-quarter results on June 23, with revenue of $25.0 billion and adjusted operating income of $2.09 billion. Capital spending as a percentage of revenue fell to 4.0%, the lowest annual level in FedEx history. That result provided a clean positive signal on logistics and goods demand that the tech-driven market narrative largely ignored on the same day it was delivered.

The VIX at 19.49 and What It Means

The Cboe Volatility Index rose 12.79% to 19.49 on June 23, a level that reflects genuine uncertainty rather than panic. A VIX above 20 typically signals elevated institutional hedging activity. The current reading below that threshold suggests markets are repricing risk rather than fleeing it entirely.

Investors watching the June 24 Micron report should treat the elevated VIX as a signal that the earnings reaction, in either direction, will be amplified beyond what the fundamental numbers alone would generate in a lower-volatility environment.