Nano Nuclear Energy (NNE) is riding one of Wall Street’s hottest emerging themes: small modular reactors, or what Nano itself calls microreactors. Long overshadowed by better-known names like Oklo and NuScale Power, Nano has started pulling attention away from both thanks to a cheaper valuation and steady regulatory progress.

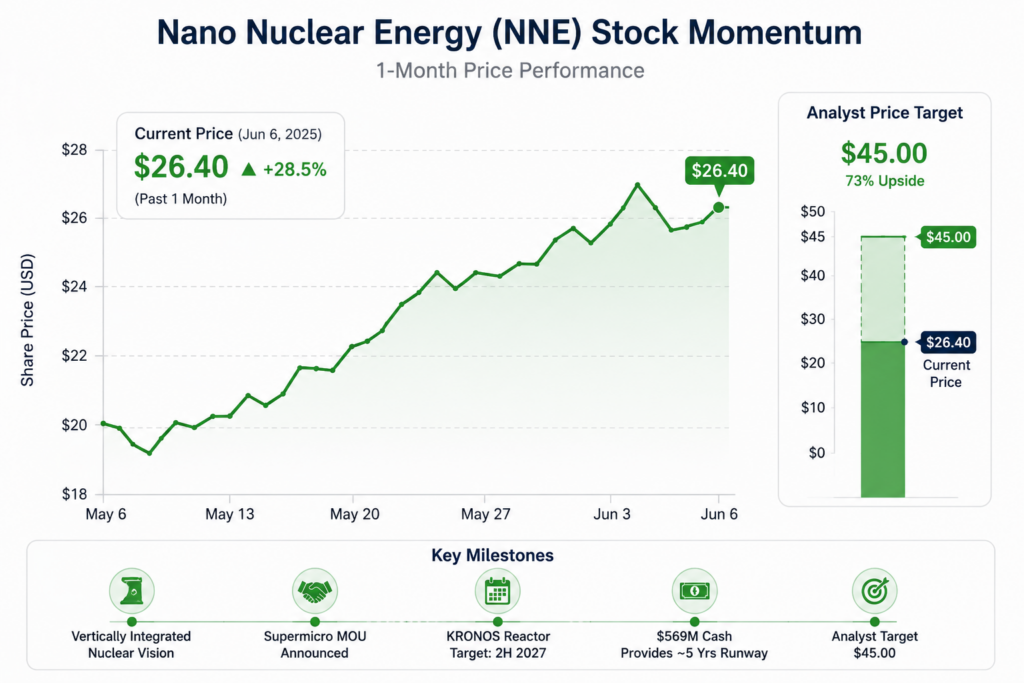

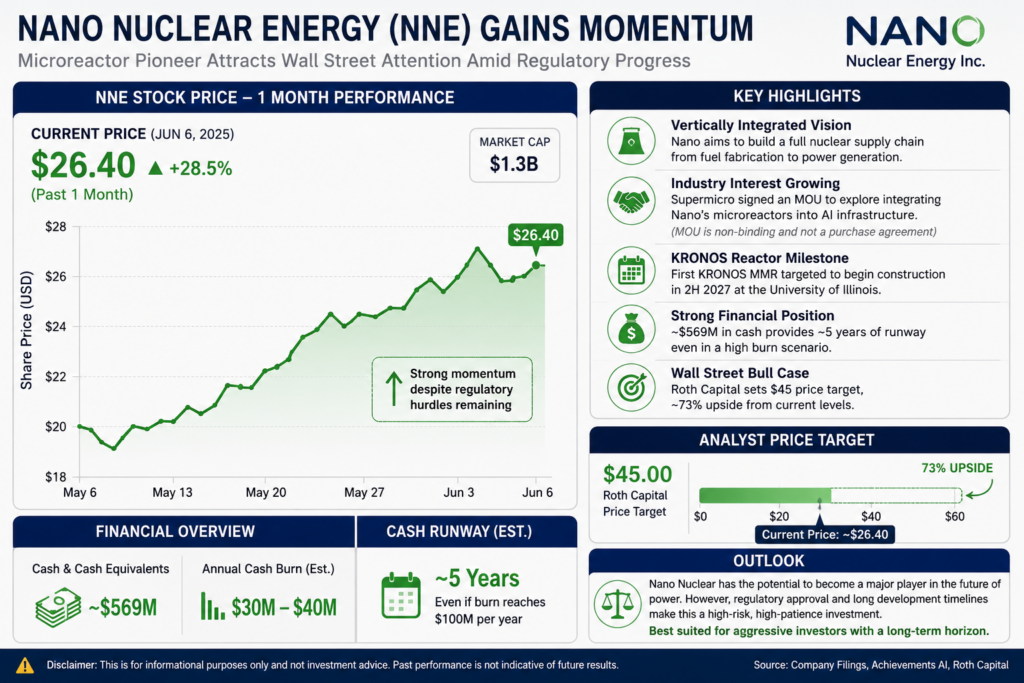

The stock has been gaining momentum over the past month, even though the central obstacle to its progress, the lack of regulatory approval, hasn’t actually changed. At a $1.3 billion valuation and a share price hovering between $26 and $27, the stock sits at an interesting crossroads.

Analysts from Achievements AI explored whether the current setup presents a compelling long-term opportunity or if investors would be better served waiting for greater execution certainty.

The Vertically Integrated Nuclear Empire Nano Wants to Build

Nano’s ambitions go well beyond certifying a single reactor design. The company is aiming to build a vertically integrated nuclear business, not just constructing and deploying microreactors, but also participating in fuel fabrication, transportation, and other links in the nuclear supply chain.

If that vision plays out, Nano’s microreactors could end up powering everything from rural data centers to military bases, or even lunar and deep-sea operations, with revenue flowing in through long-term power purchase agreements (PPAs).

Big Names Are Already Circling

Even though microreactors remain unproven at commercial scale, interest from larger industry players is already beginning to emerge. In May, Super Micro Computer signed a memorandum of understanding (MOU) with Nano to explore the potential integration of microreactor technology into Super Micro’s AI infrastructure offerings.

Importantly, an MOU is not a binding purchase agreement, and it does not guarantee future revenue. However, the announcement serves as a meaningful signal that established technology companies are actively evaluating how advanced nuclear solutions could support the rapidly growing power demands of AI data centers.

For Nano, the agreement provides early validation of market interest. If the company’s reactor designs successfully clear regulatory certification and move toward commercialization, preliminary partnerships like this could evolve into formal supply agreements, deployment contracts, or broader strategic collaborations.

While the opportunity remains speculative today, the Supermicro relationship suggests that demand could materialize quickly once the technology becomes commercially viable.

The KRONOS Reactor: 2027, If the Regulators Cooperate

Nano’s nearest-term milestone is its first KRONOS micro modular reactor (MMR), with construction targeted to begin in the second half of 2027 a timeline that depends entirely on smooth progress through regulatory approvals. The reactor is slated for construction at the University of Illinois Urbana-Champaign, roughly 100 miles from the site of the Chicago Pile-1, the first nuclear reactor ever built in the U.S.

That historical proximity is a nice narrative touch, but it doesn’t change the fact that regulatory approval remains the single biggest variable standing between Nano and an actual operating reactor.

The Cash Cushion That Buys Nano Time

One factor working strongly in Nano’s favor is that the company is not facing any immediate financial pressure. While it currently generates minimal revenue, it holds approximately $569 million in cash and cash equivalents, providing a substantial financial cushion as it advances its programs.

Even under a conservative stress-test scenario where annual cash burn reached $100 million, well above its current estimated rate of $30 million to $40 million per year, Nano would still have enough liquidity to fund operations for roughly five years without raising additional capital.

That strong balance sheet gives the company a meaningful advantage. It provides ample runway to navigate regulatory reviews, continue development efforts, and pursue commercialization opportunities without the urgency that often forces early-stage biotech companies into dilutive equity offerings. For investors, the cash position reduces a key risk factor by allowing Nano to focus on execution rather than near-term financing needs.

Wall Street’s Bull Case: A $45 Price Target

The Street is paying attention too. An analyst at Roth Capital recently set a price target of $45 on Nano shares, implying roughly 73% upside from the current price near $26. That’s an aggressive call, and it reflects genuine optimism about Nano’s long-term positioning in the microreactor space, but it’s also a target built on a technology and regulatory pathway that hasn’t been proven out yet.

Outlook: A High-Risk, High-Patience Bet

Nano Nuclear has the ingredients to become a meaningful electricity supplier someday: a differentiated reactor design, early interest from major tech infrastructure players, and enough cash to survive a long regulatory slog.

But “someday” is the operative word: realizing that potential could easily take a decade or more, and by then, the energy landscape, competing SMR designs, policy shifts, and alternative power sources could look meaningfully different from today’s setup, potentially diminishing what makes Nano exciting right now.

Given that uncertainty, this remains a stock suited for aggressive investors willing to take a calculated bet on a still-nascent industry. Investors with lower risk tolerance may be better served by a nuclear energy ETF that holds Nano alongside more established names, capturing the theme without concentrating the bet on a single, pre-revenue company.