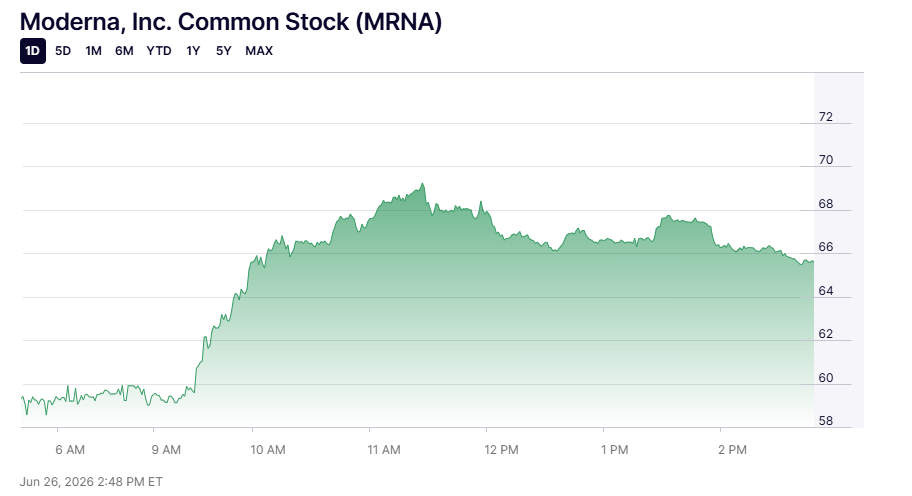

Moderna (MRNA) shares jumped roughly 14% today, touching a fresh 52-week high near $69.29 before settling into the high $60s. That move dwarfs the gains posted by vaccine peers Merck and Pfizer, both up closer to 2% on the same day.

Brokers from Achievements AI looked into what’s actually driving the rally, and whether the move is backed by fundamentals or running ahead of them.

The FDA Vote That Started It All

The clearest catalyst sits in the rearview mirror but is still fueling momentum. An FDA advisory committee voted 9 to 0 to back Moderna’s flu vaccine candidate, known as mRNA-1010 or mFlusiva, for adults aged 50 to 64 and 65 and older.

A unanimous panel vote is a strong signal heading into the official PDUFA decision date of August 5, 2026, and if cleared, it would become Moderna’s fifth approved product. For a company still searching for a commercial pillar beyond COVID vaccines, that’s a meaningful de-risking event.

Science Day Added Fuel: Moderna’s Pivot Beyond Vaccines

The rally received another boost following Moderna’s Science Day event, where management presented a broader vision that extends well beyond its traditional infectious disease business.

The company highlighted encouraging progress across several pipeline programs, including oncology, autoimmune disease, a T-cell engager platform, an in vivo CAR-T therapy, and a treatment for propionic acidemia. Together, these initiatives demonstrate Moderna’s continued investment in expanding the applications of its mRNA technology.

Management also announced plans to increase manufacturing capacity in Germany, including the potential acquisition of facilities that BioNTech is reportedly considering closing. This signals the company’s ambition to significantly expand production capabilities as its pipeline matures.

Although none of these programs are generating commercial revenue today, they support Moderna’s transformation into a diversified mRNA platform company rather than a business primarily associated with COVID-19 vaccines.

Investor optimism suggests the market is increasingly assigning value to Moderna’s long-term pipeline and future growth potential, rather than focusing solely on its current revenue base.

The Numbers Behind the Narrative

There’s real financial momentum underneath the headlines, too. Moderna’s first quarter 2026 revenue came in at $389 million, up 264% year over year and beating consensus estimates by roughly 65%. The company also reaffirmed guidance calling for up to 10% revenue growth in 2026, a notable shift in tone for a company that’s been working through a steep post-pandemic revenue decline.

Wall Street Isn’t Fully Convinced Yet

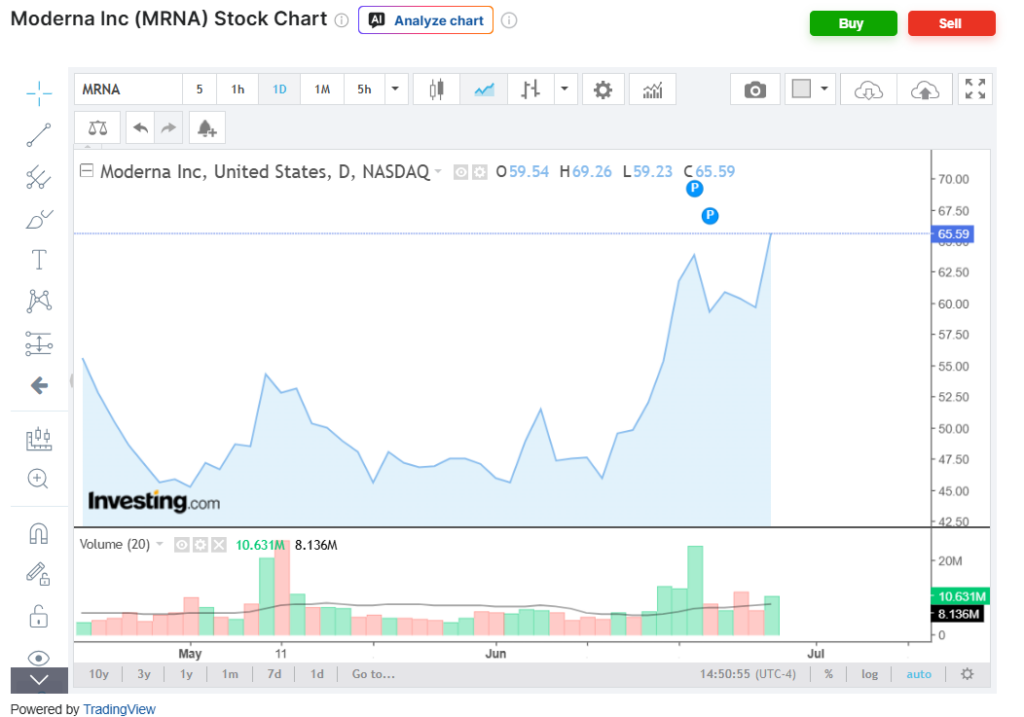

Valuation concerns continue to temper the bullish narrative despite Moderna’s impressive rally. Although the stock is up roughly 130% year to date, Wall Street’s consensus price target is just $43.45, well below its current trading price.

Even after the positive FDA advisory vote, Jefferies raised its target to $53 but maintained a Hold rating, arguing that meaningful flu vaccine revenue is unlikely before 2027. Other analysts remain even more cautious, with Leerink’s target near $24 and Morgan Stanley’s around $33, both suggesting limited upside from current levels.

Another factor drawing attention is insider selling. Company executives have recently recorded approximately 75 net-selling transactions, indicating more selling than buying. While insider sales alone do not invalidate the long-term investment case, they add another layer of caution.

Combined with a forward price-to-earnings ratio of around 23, despite earnings that remain dependent on future pipeline success, the stock’s recent gains appear to be driven more by investor optimism and momentum than by firmly established near-term fundamentals.

Outlook

Moderna’s recent rally is supported by a meaningful regulatory milestone and a significantly stronger long-term growth narrative than the company has presented in recent years.

Positive momentum following the FDA advisory committee vote, combined with growing confidence in its diversified mRNA pipeline, has reignited investor optimism. The company’s expansion into oncology, autoimmune diseases, and next-generation therapies has also strengthened the perception that Moderna is evolving beyond its dependence on COVID-19 vaccines.

However, the gap between the stock’s current price and most Wall Street price targets remains substantial, suggesting the recent advance may be driven more by momentum and improving sentiment than by near-term fundamentals. While investors are increasingly pricing in the company’s future potential, many analysts believe it will take several years before these pipeline programs generate meaningful commercial revenue.

The next major catalyst will be the FDA’s PDUFA decision on August 5. That ruling is expected to play a critical role in determining whether the recent rally can continue. A positive outcome could reinforce confidence in Moderna’s long-term strategy and support further gains, while disappointment may trigger profit-taking after the stock’s strong run.

How shares perform before and immediately after the decision will provide valuable insight into whether investor enthusiasm is supported by fundamentals or has moved ahead of the company’s near-term outlook.