The international foreign exchange ecosystem is witnessing extreme architectural stress as the primary East Asian currency undergoes a prolonged valuation contraction against its North American counterpart.

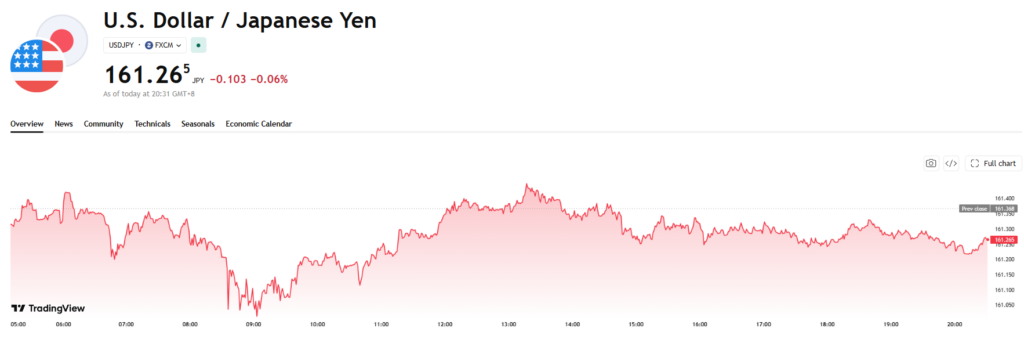

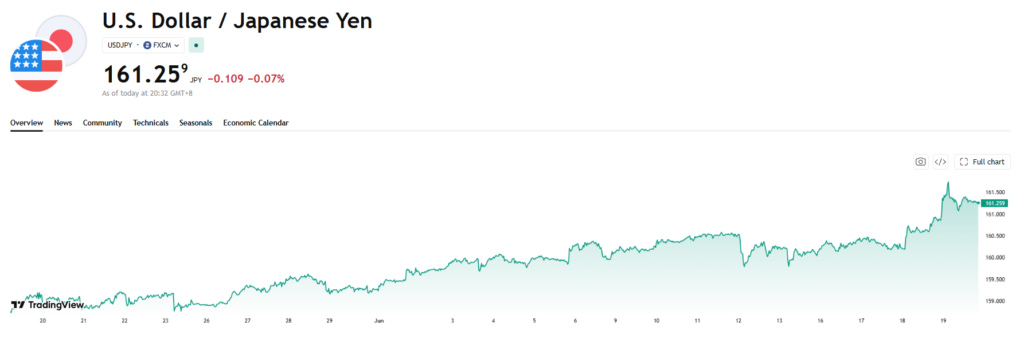

Investment researchers at Kepler Group notes that the major currency pair is hovering aggressively near historic multi-decade thresholds, rapidly approaching its previous cyclical peak of approximately 162.00. Prominent European banking researchers emphasize that further upward velocity is highly probable, while counterpart institutional desks warn that official regulatory rhetoric is intensifying as spot prices match historical depths.

The current currency depreciation trajectory has pushed the asset within striking distance of its weakest valuation since 1986, triggering widespread capital market anxieties. Strategic macro strategists highlight that a scheduled lull in global trading activity could offer fiscal regulators a pristine tactical window to execute a surprise market intervention.

This localized liquidity vacuum introduces severe structural risks, meaning that further currency declines are highly likely to provoke immediate, aggressive defensive positioning from official capital authorities.

Sovereign currency traders are heavily focused on this regulatory wild card, which possesses the absolute capacity to trigger sharp, high-velocity market reversals with minimal warning. While the broader macroeconomic trend fundamentally supports sustained greenback dominance, the sheer proximity to historic multi-decade lows makes unilateral market stabilization highly attractive to fiscal ministries.

Consequently, institutional desks are advising extreme caution, bracing for sudden bursts of cross-border volatility as trading desks balance organic macroeconomic momentum against artificial regulatory barriers.

Technical Momentum Paths And Ascending Support Infrastructure

From a purely structural chart perspective, the asset class has convincingly reestablished its broader upward trajectory after successfully defending an enduring multi-month ascending trendline. The spot rate recently cleared the upper resistance boundary of its previous consolidation matrix, validating the overwhelming strength of the current buying cycle.

Technical research groups identify the 2024 peak near 162.00 as the primary near-term ceiling that macro allocators must breach to unlock secondary expansion targets.

A clean, sustained breakout above that historical high-water mark would fundamentally expand the asset’s structural parameters, exposing measured-move objectives well beyond 164.00. This technical reality would leave the domestic currency under immense selling pressure, forcing cross-border corporations to actively hedge their localized cash allocations.

The market’s current path underscores a broad-based structural imbalance where programmatic buyers consistently overwhelm defensive capital flows during active trading sessions.

Diverging Macro Risk Parameters And Sovereign Defense Zones

While global financial institutions uniformly agree that the underlying currency remains structurally exposed, they diverge on immediate operational risk models.

Leading French investment banks favor an extended continuation of the upward vector, contingent on the asset successfully preserving a critical support zone clustered between 159.65 and 159.10. If these technical baselines hold firm, institutional targets are projected to advance sequentially toward 163.70, 164.20, and eventually 165.70.

Conversely, German banking analysts prioritize the rising probability of an unannounced regulatory liquidity injection near the historic 1986 baselines. This operational divergence creates a highly complex environment for tactical foreign exchange funds operating across global financial hubs.

Ultimately, the tension between sustained technical momentum and imminent sovereign defense initiatives ensures that near-term price discovery will remain a highly volatile, discontinuous process.

Liquidity Threshold Variables And Corporate Hedging Demands

The ongoing contraction of the East Asian asset is exerting significant operational pressure on international manufacturing conglomerates reliant on predictable localized input costs. Importers operating within the region face severe margin degradation as the real purchasing power of the domestic currency collapses relative to international standards.

This structural devaluation is forcing corporate treasuries to aggressively deploy advanced forward contracts and options structures to protect their balance sheets from unmitigated downside exposure.

Furthermore, the structural failure of previous verbal interventions to alter the broad macroeconomic trajectory suggests that only direct, high-volume capital deployment can achieve a permanent trend reversal. However, executing large-scale asset stabilization requires substantial reserves of foreign liquid capital, introducing a secondary layer of fiscal complexity for domestic regulators.

Multipolar Currency balancing and Long-Term Macro Realignment Options

Looking forward into the concluding quarters of the current fiscal period, the ultimate trajectory of the pair will depend on the widening monetary policy gap between global capitals.

If overseas central banks maintain a highly restrictive, high-yield environment while the local monetary authority pursues ultra-loose parameter models, organic capital flight will continue unabated. Tactical portfolio managers are structuring their multi-asset frameworks to capitalize on this systemic yield differential, treating any minor currency corrections as favorable entry thresholds.

The prolonged weakness of a primary tier-one asset complicates capital redistribution for sovereign wealth funds managing massive multi-polar currency reserves. The structural decline of a major global wealth repository changes global multi-asset model baseline risk assumptions.

These institutional giants’ portfolio rebalancing will cause capital migrations across global fixed-income, commodity, and equity matrices, redefining international value accumulation for years.