US stock futures opened in mixed territory on June 22, 2026, with Dow futures slipping and oil prices easing as the first full day of US-Iran peace negotiations in Switzerland got underway. S&P 500 futures were down 0.2%, while Nasdaq futures edged slightly positive ahead of a week that will deliver earnings from Micron, FedEx, and Carnival alongside May PCE inflation data.

A financial expert at Bankolla underlines that what markets are reading on June 22 is not a single-event story but a multi-variable setup where geopolitics, inflation data, and corporate earnings are all converging inside the same five-day window.

What Oil Is Telling the Market on June 22

Crude oil’s behavior on June 22 is one of the more instructive market signals of the day. Oil eased slightly with Brent near $81 per barrel as Iran’s foreign minister stated there had been major progress in the Swiss negotiations toward ending the conflict permanently.

That language, coming from the Iranian side, is the strongest official confirmation yet that the ceasefire framework signed in France is holding and progressing toward a durable agreement.

For equity markets, lower oil feeds through multiple channels simultaneously. Energy sector stocks face near-term revenue pressure as prices retreat. But technology, consumer, and industrial stocks benefit from the inflation relief that cheaper crude delivers into the PCE and CPI pipeline.

The net effect on the S&P 500 from an oil decline of this type tends to be modestly positive because the index is far more weighted toward technology and consumer names than energy.

The Week’s Earnings Lineup and What It Signals

The earnings schedule for the week of June 22 is unusually information-dense for a mid-summer period. FedEx reports Tuesday, Micron reports Wednesday, and Carnival Corporation reports alongside additional names later in the week. That combination provides simultaneous reads on logistics demand, AI memory supply chains, and consumer discretionary travel spending.

Collectively, those three reports answer whether the economy is genuinely absorbing the Iran war’s inflationary impact without a meaningful demand slowdown.

If FedEx shows stable parcel volumes, Micron confirms HBM demand remains fully allocated, and Carnival reports strong forward booking trends, the picture that emerges is an economy that has handled a significant geopolitical shock better than many models predicted.

Iran Talks and the Stocks Most Sensitive to Resolution

The US-Iran peace negotiations in Switzerland are being watched closely by specific equity sectors most directly affected by the conflict’s economic consequences. Airline stocks, which had rallied strongly on June 15 after the initial ceasefire framework emerged, are sensitive to any breakdown in talks that would reintroduce fuel cost uncertainty for carriers benefiting from oil’s retreat.

Energy stocks face a different dynamic. Companies like Diamondback Energy and other oil-focused names had been among the best performers during the conflict’s peak and are now facing the reverse pressure as peace reduces the geopolitical premium that had supported crude prices above $100. That sector rotation from energy into technology and consumer names is already visible in the premarket movers on June 22.

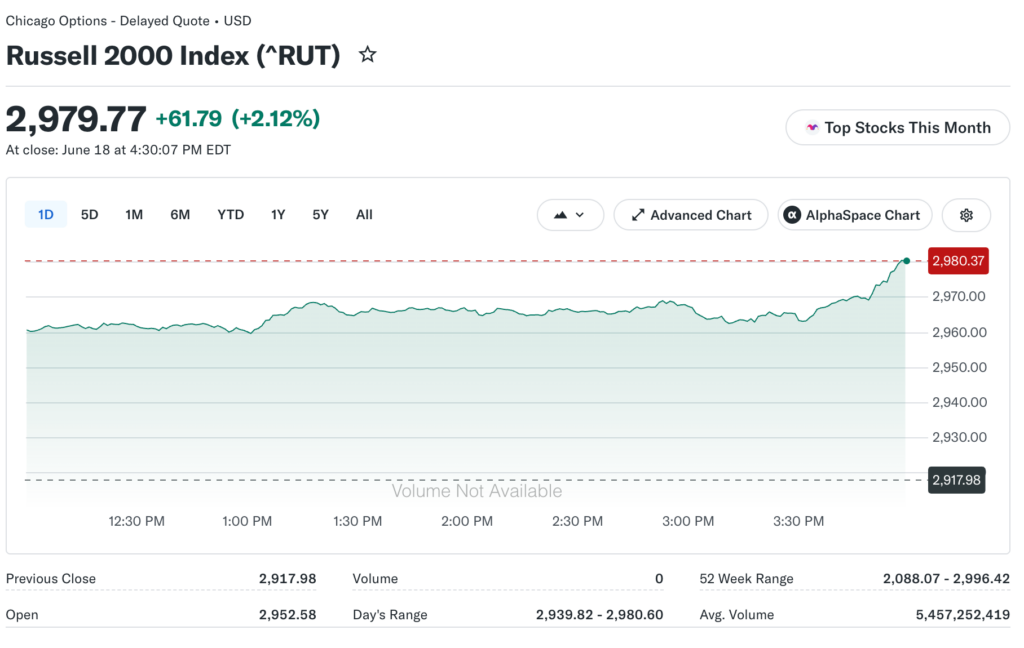

Why the Russell 2000 Is the Breadth Indicator to Watch

The Russell 2000 closed at 2,979.77 at the end of the prior week, up 2.12% on June 18 in the session following the Fed’s hawkish hold. Small-cap strength on a day when the Fed signals potential rate hikes is counterintuitive, and the Iran ceasefire relief explains most of it. Lower oil reduces input cost pressure on smaller domestic businesses that have less pricing power than large-cap multinationals.

Heading into June 22, the Russell 2000 holding above 2,950 would be the clearest sign that the ceasefire-driven relief trade has staying power beyond a single session. A pullback toward 2,900 would signal that small caps are beginning to feel the weight of the hawkish Fed signal more than the benefit of lower energy costs, which would narrow market leadership back toward mega-cap technology.

The PCE Print Is the Week’s Hinge Point

Every equity sector’s direction through the remainder of June 2026 depends on what PCE inflation shows on Thursday. April’s reading came in at 3.8% annually, the highest in three years. If May’s reading confirms that the Iran war’s direct inflation contribution is beginning to fade as energy prices fall, rate expectations ease and the growth-oriented stocks that sold off sharply on June 17 have a clear path to recovery.

If PCE remains sticky above 3.5% despite lower oil, the nine FOMC members projecting a rate hike in 2026 gain more ammunition. That outcome would sustain the pressure on rate-sensitive sectors, including homebuilders and small-cap financials, that have been underperforming since the June 17 Fed decision.

The week’s outcome will be determined primarily by PCE on Thursday and secondarily by Micron on Wednesday, with FedEx providing a background read that either confirms or complicates the picture those two prints create.